CFA考試相關(guān)視頻

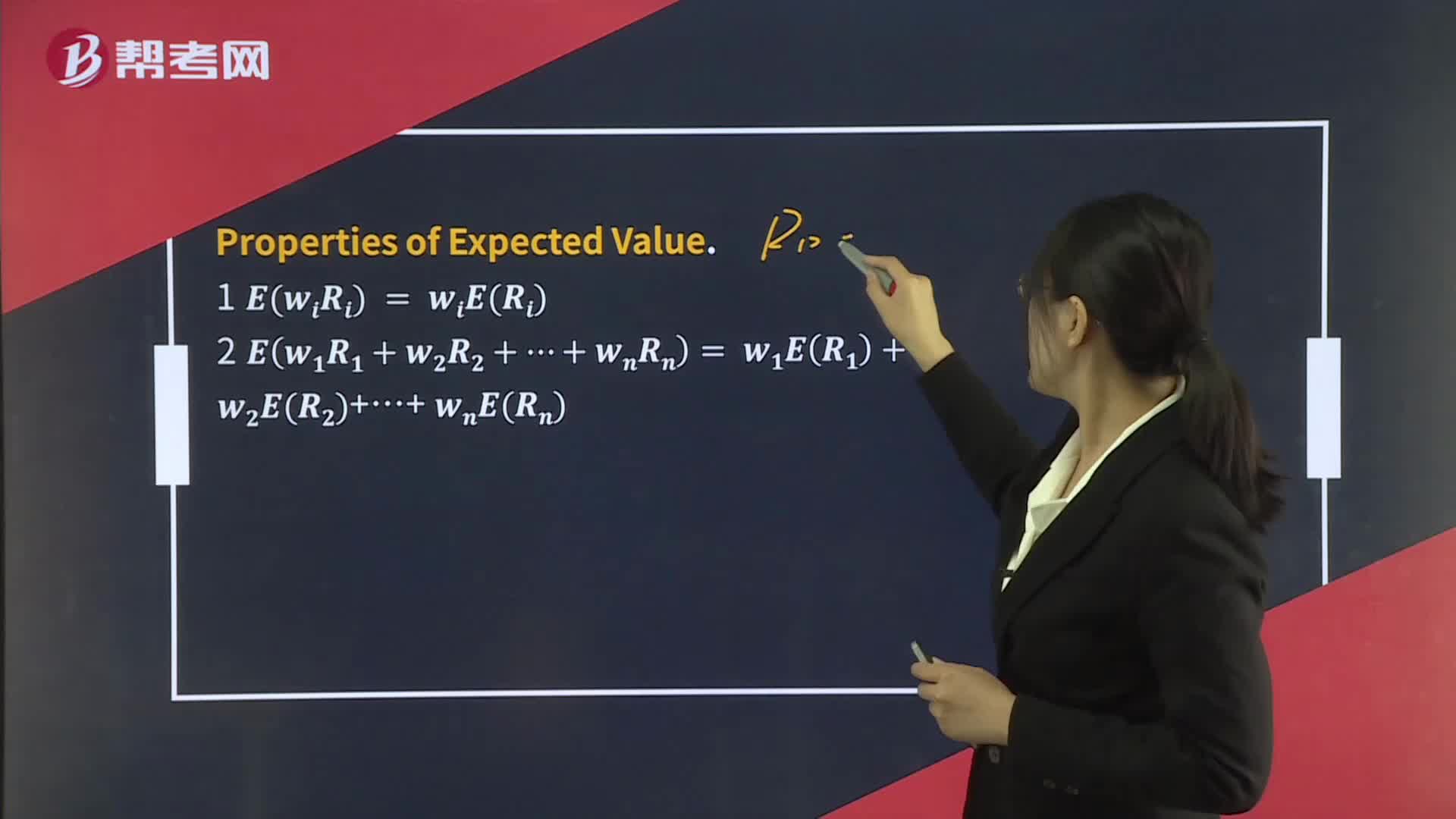

Portfolio Expected Return and Variance of Return

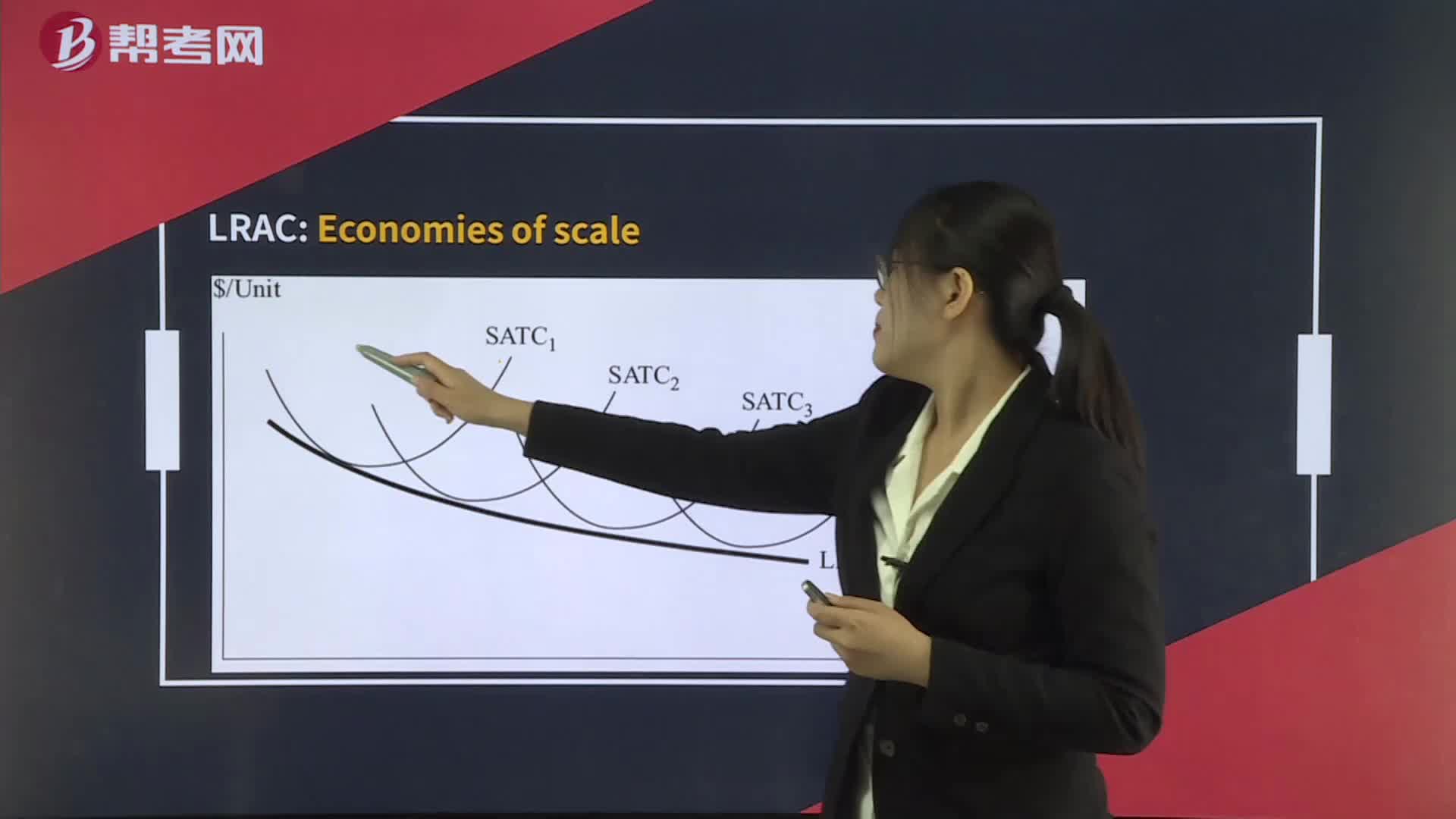

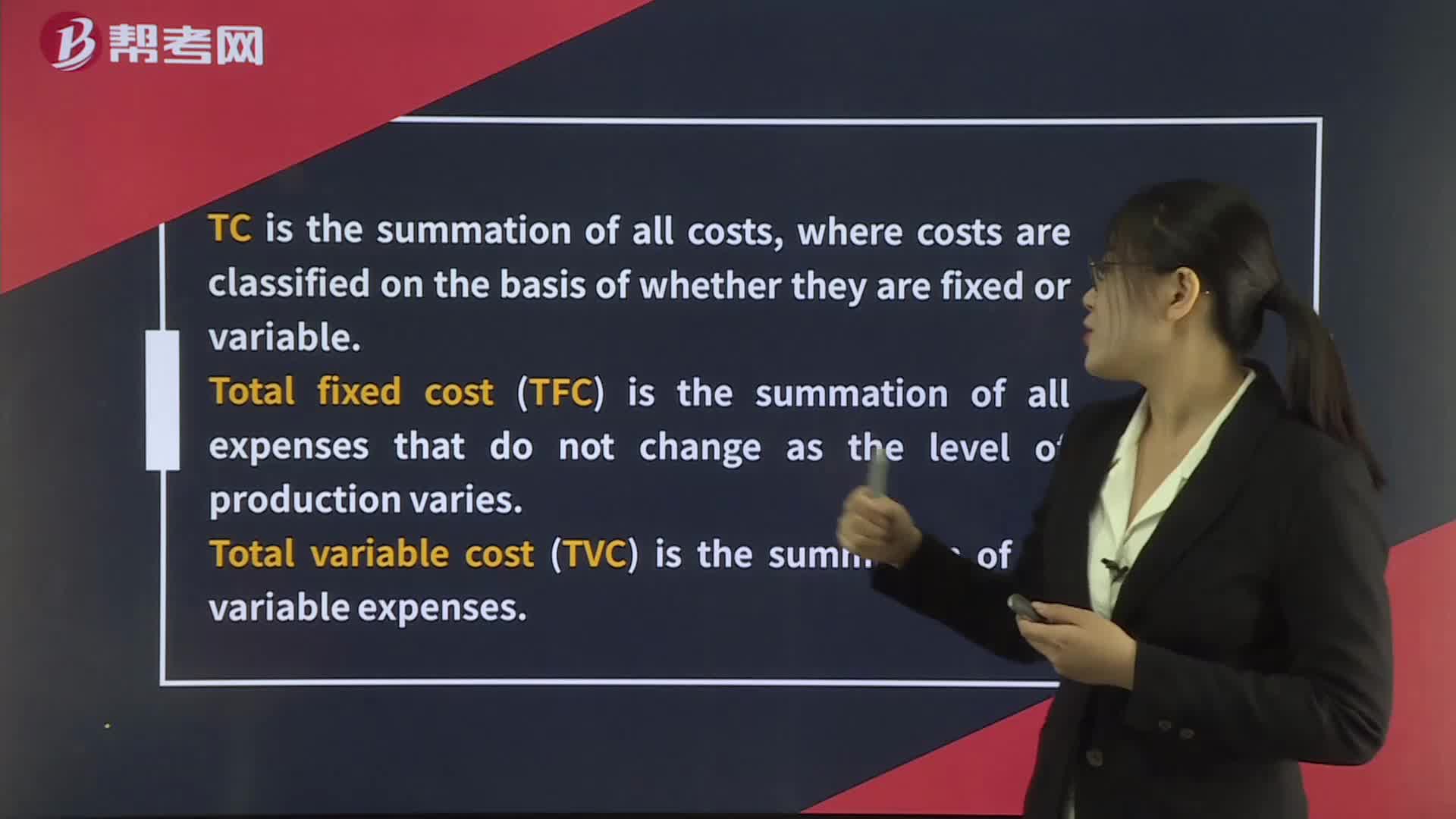

Total, Variable, Fixed, and Marginal Cost and Output

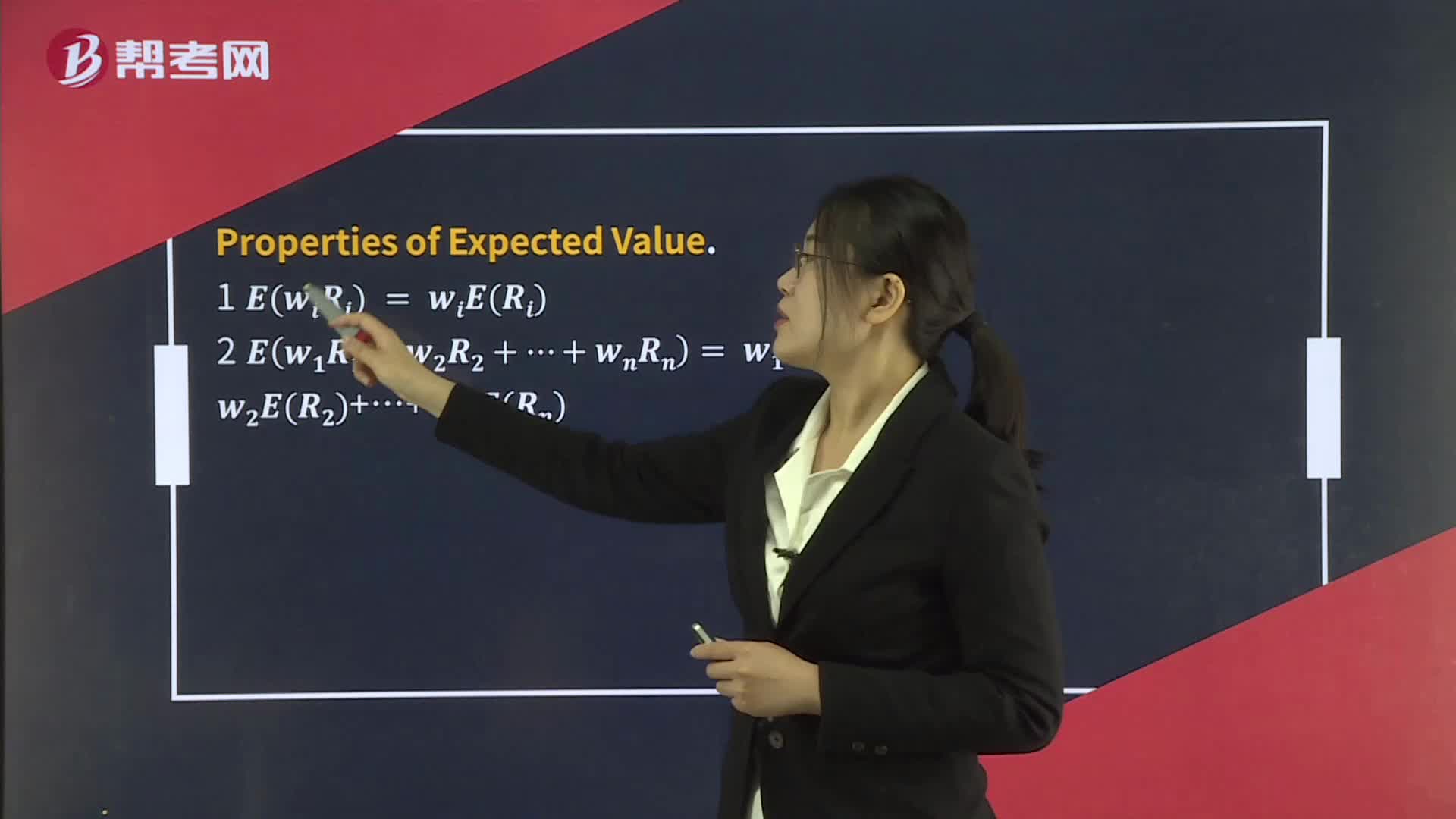

Multiplication Rule For Expected Value

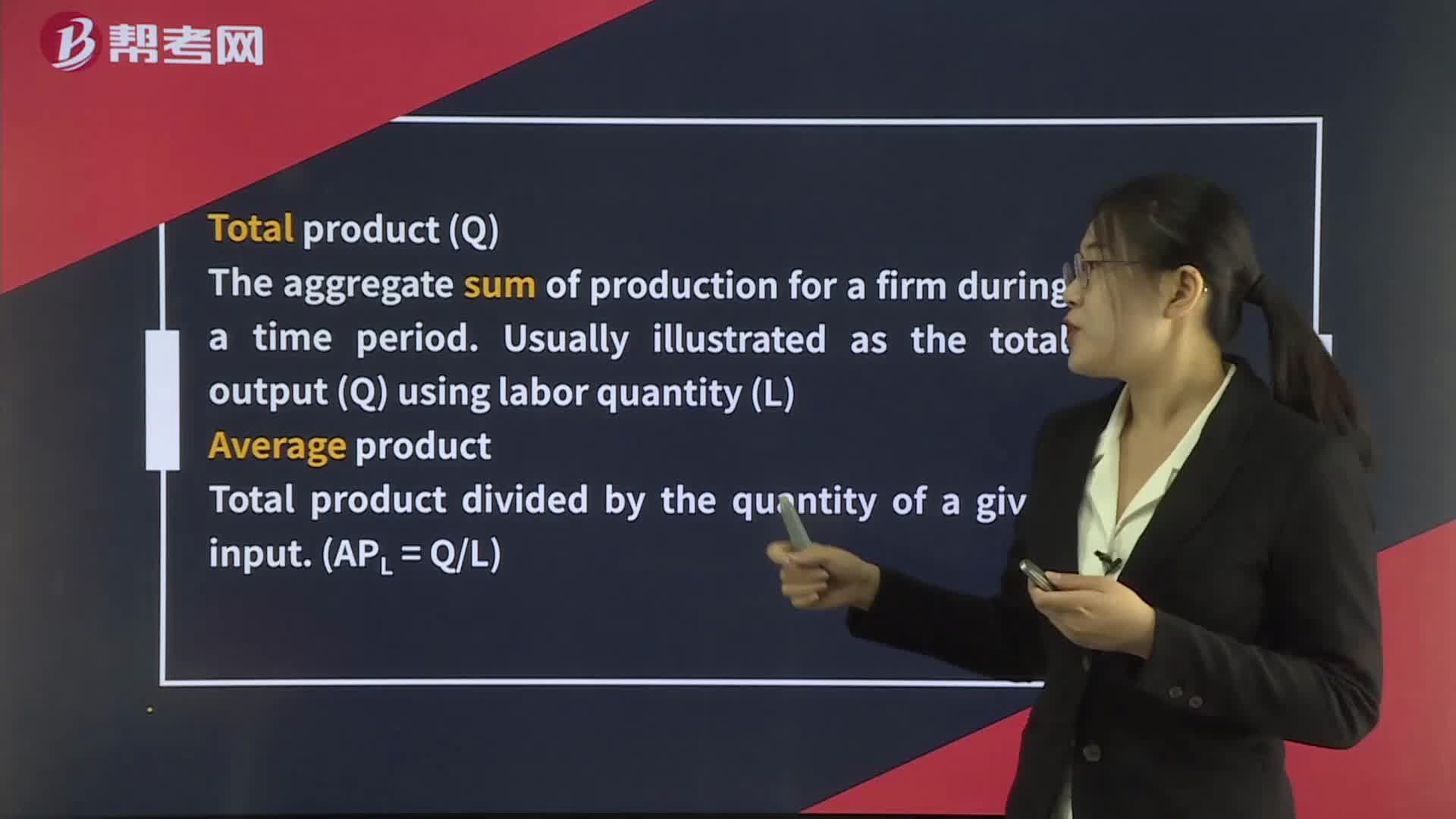

Total, Average, and Marginal Product of Labor

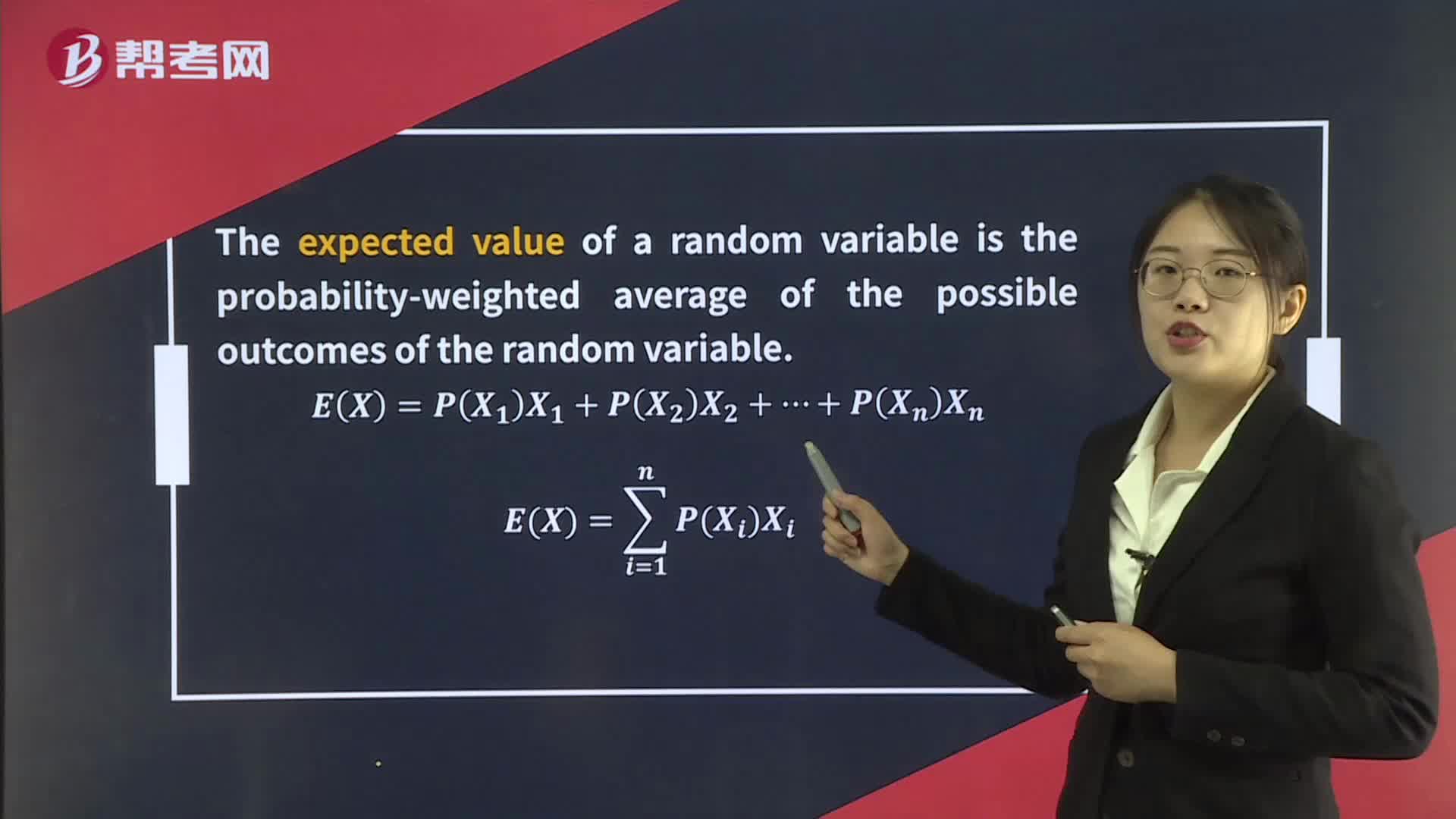

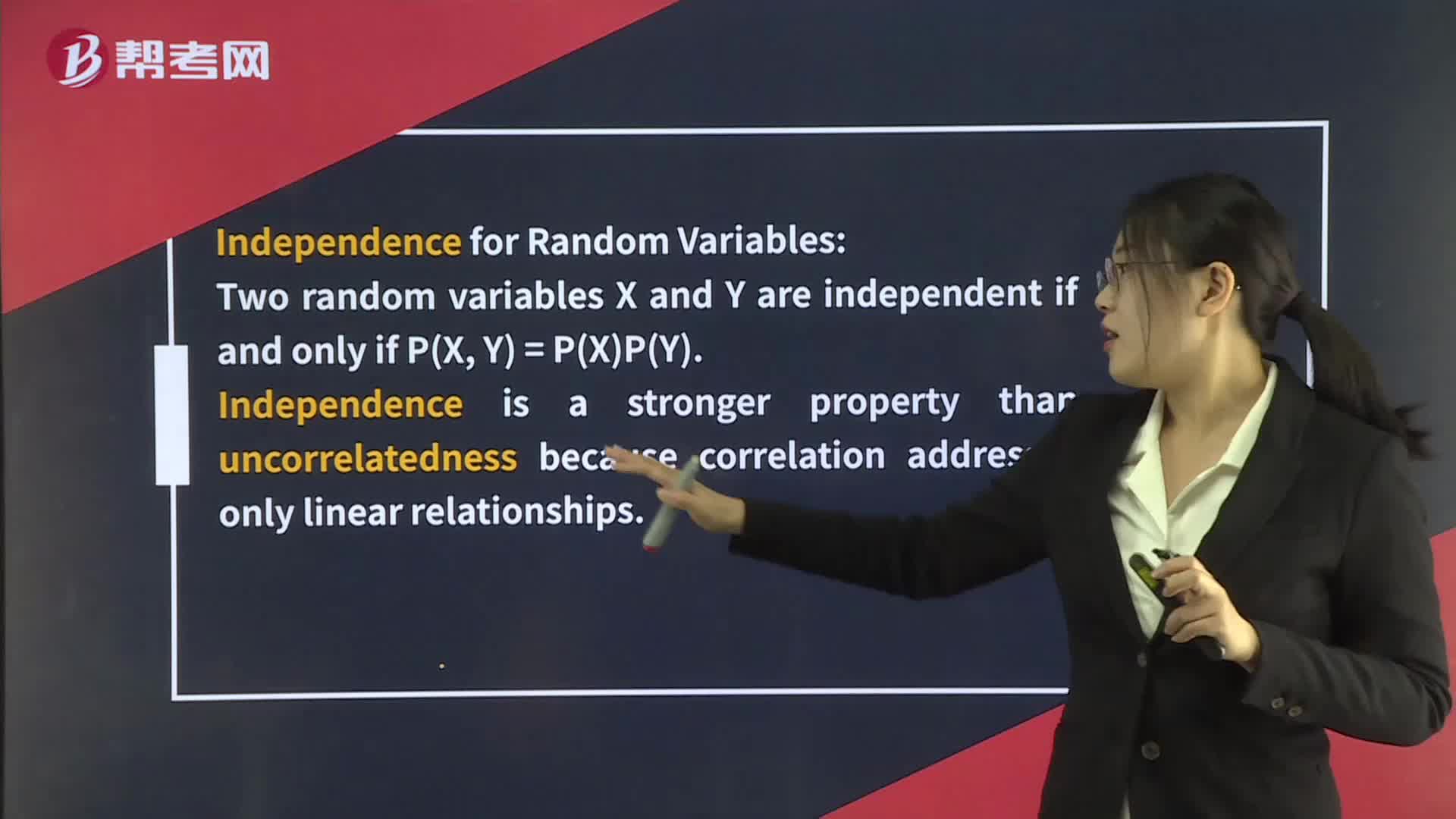

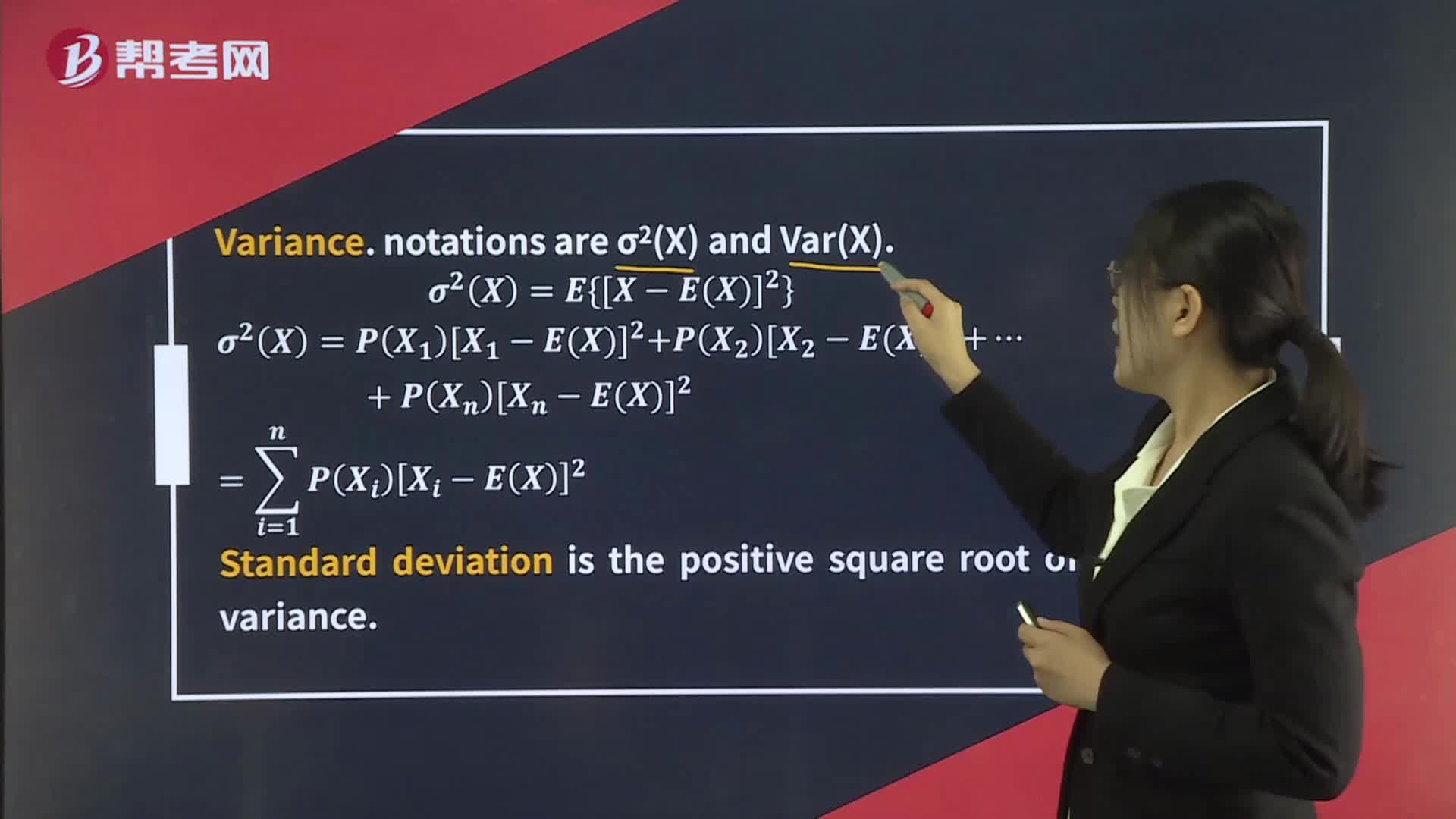

Expected Value and Variance

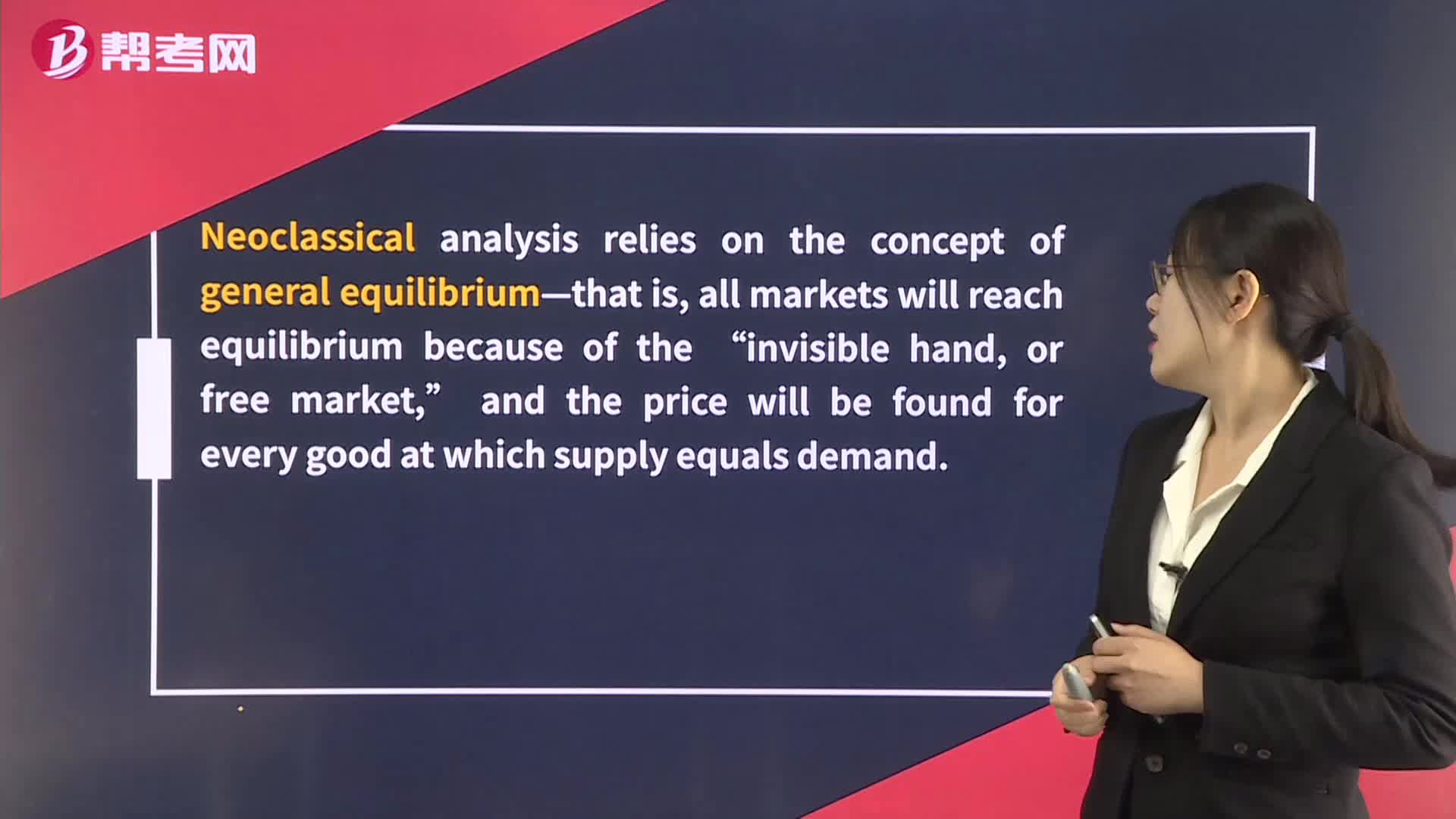

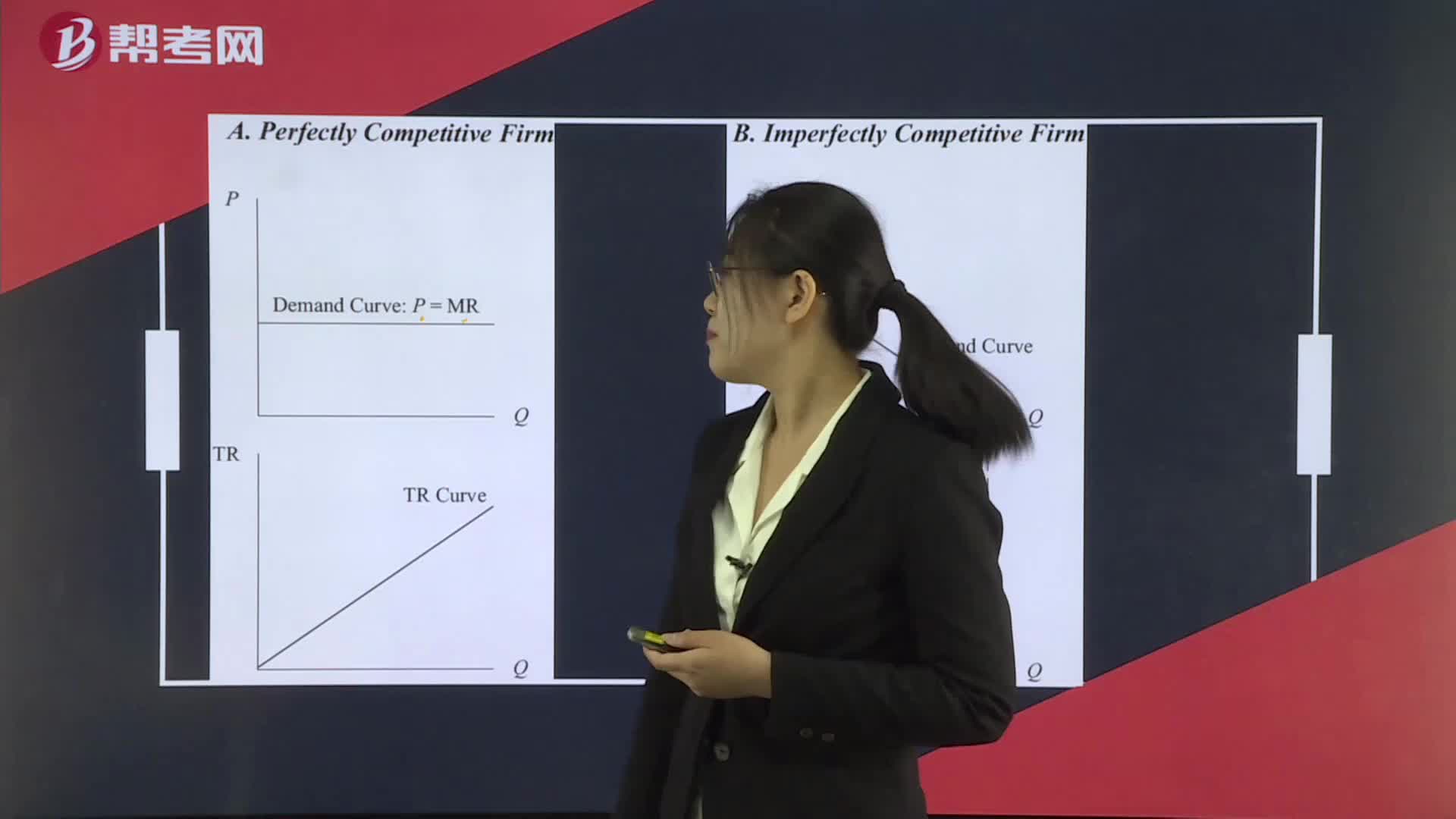

Revenue under Conditions of Perfect and Imperfect Competition

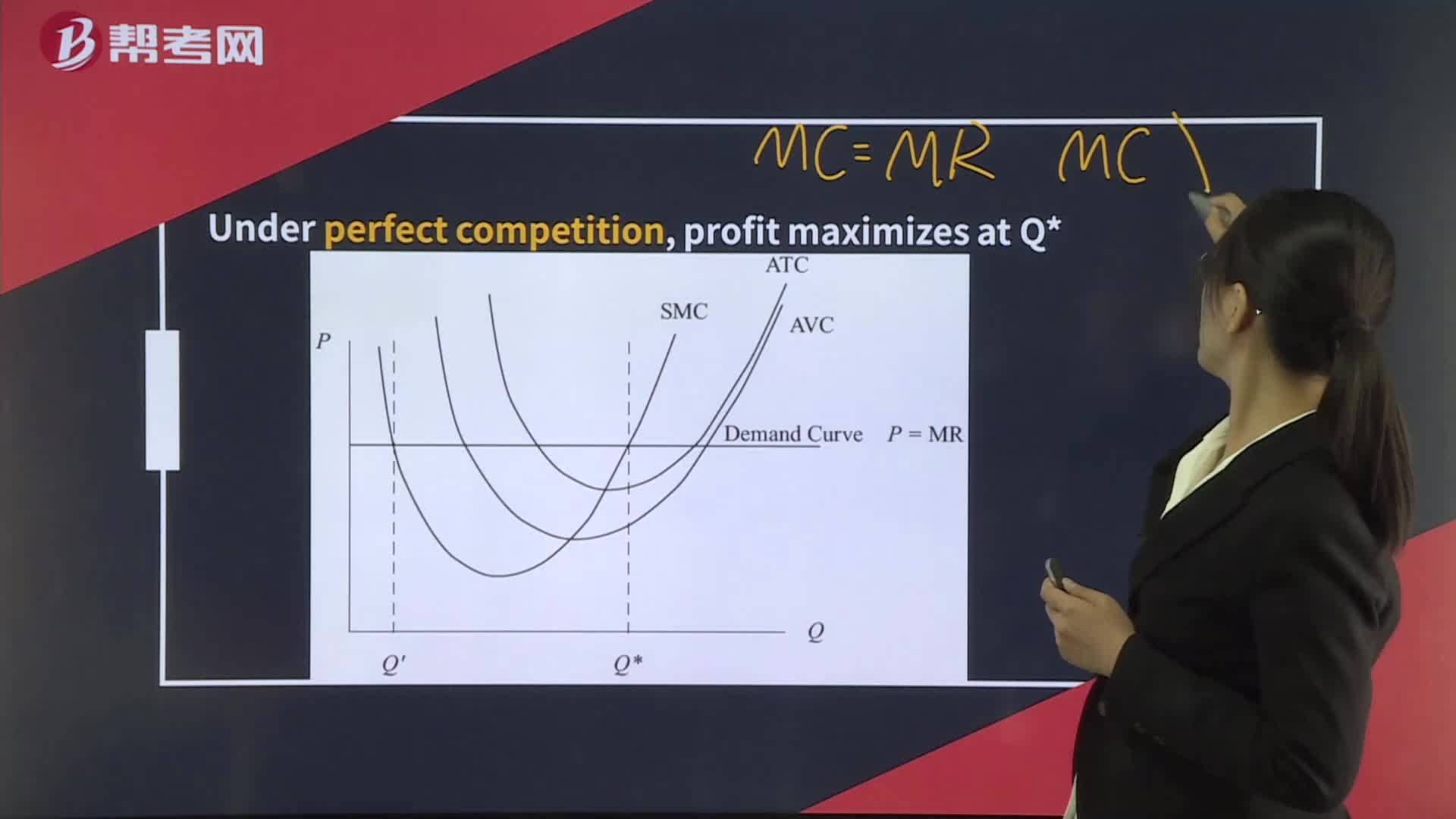

Profit-Maximization, Breakeven, and Shutdown Points of Production

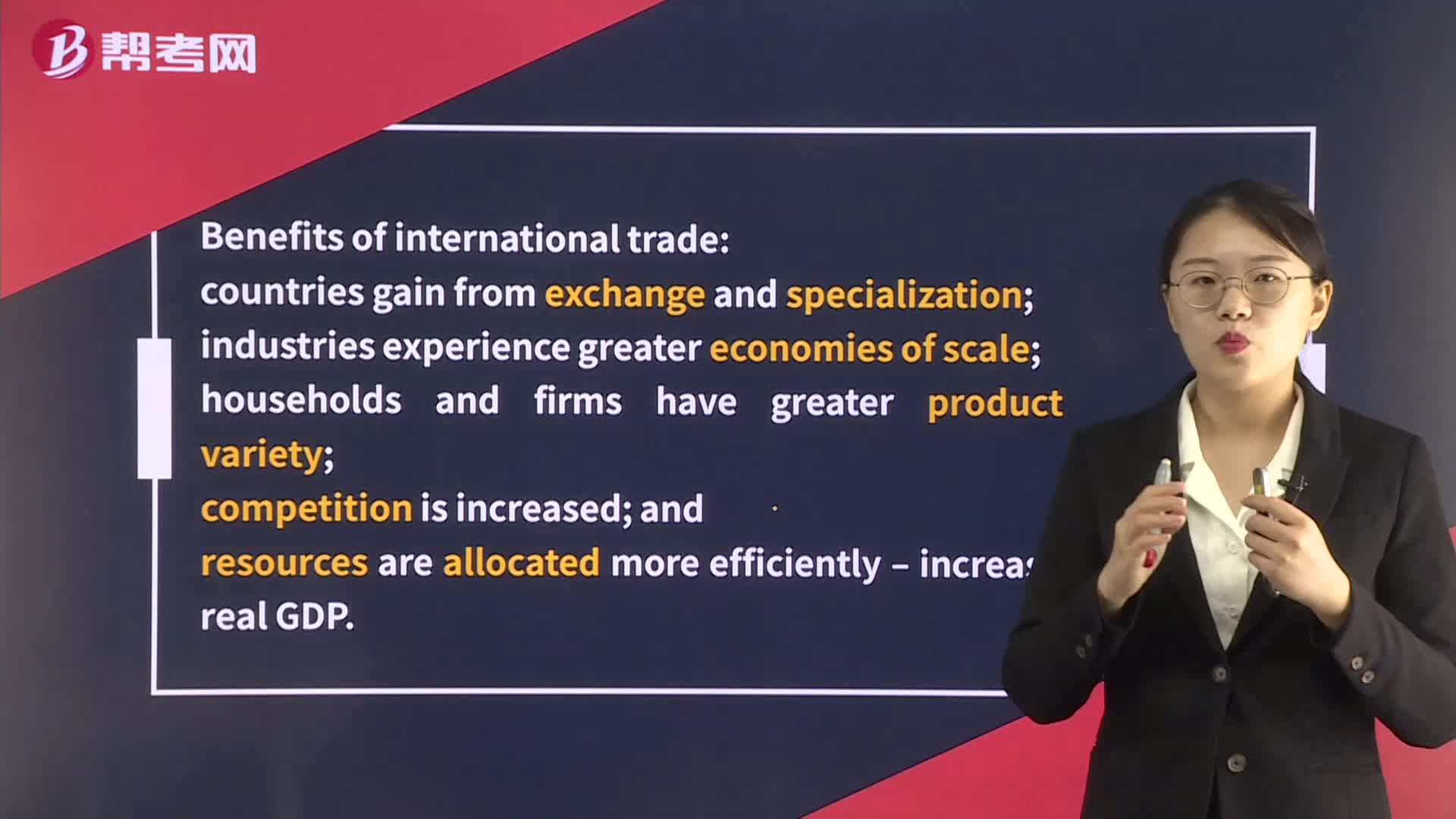

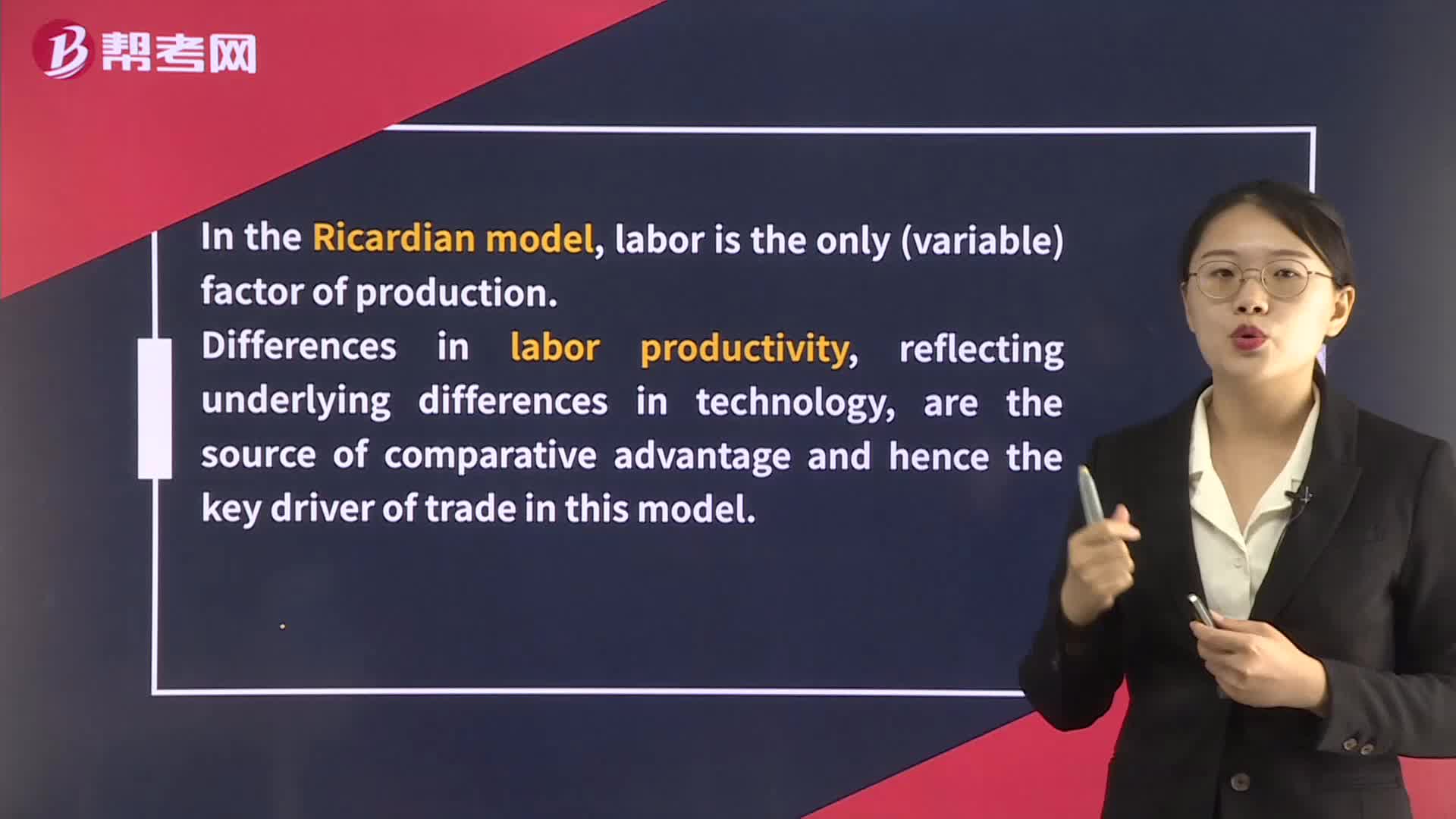

Ricardian and Heckscher–Ohlin Models of Comparative Advantage

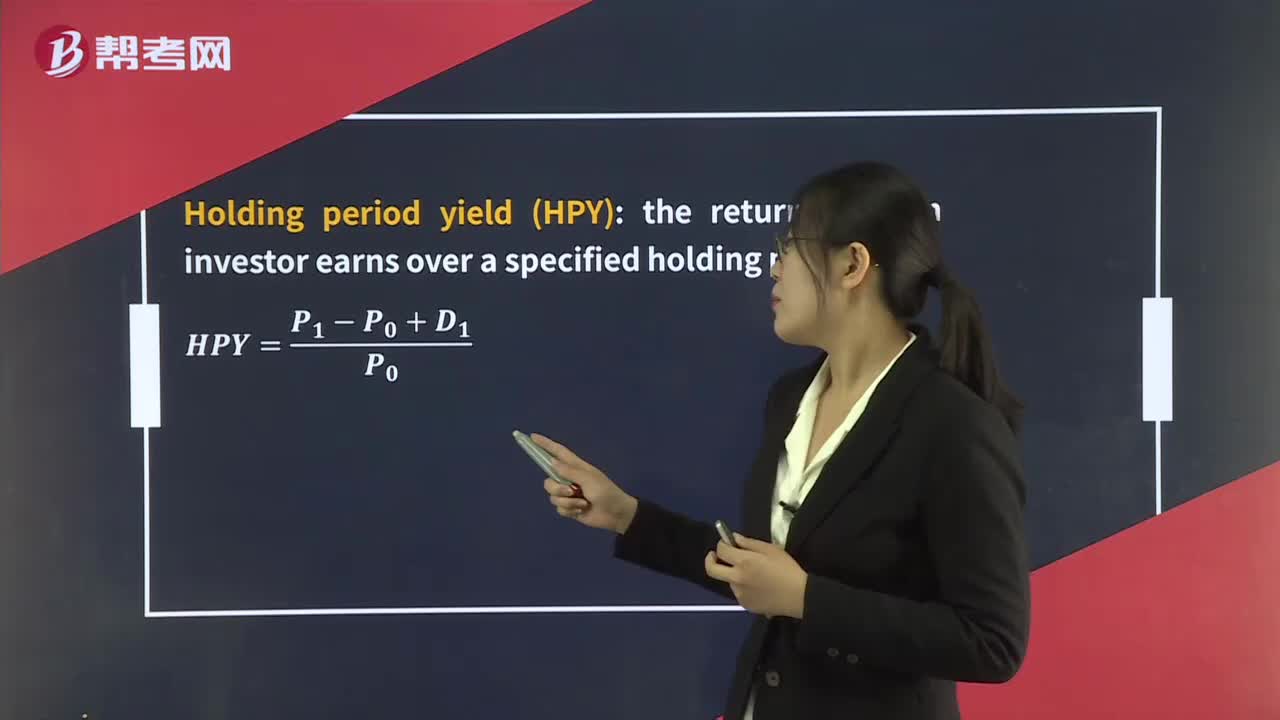

Money-Weighted Rate of Return & Time-Weighted Rate of Return

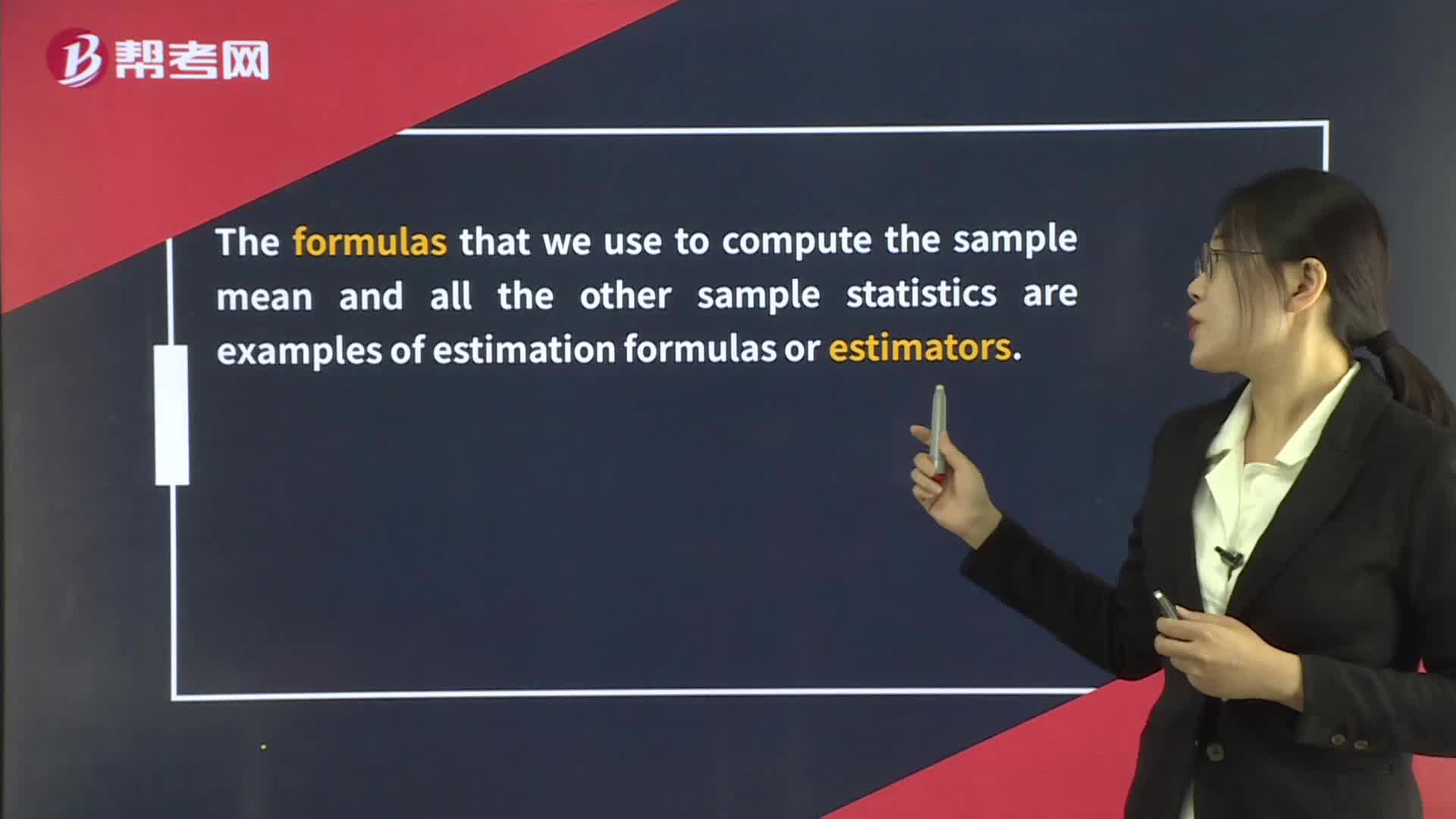

Point and Interval Estimates of the Population Mean

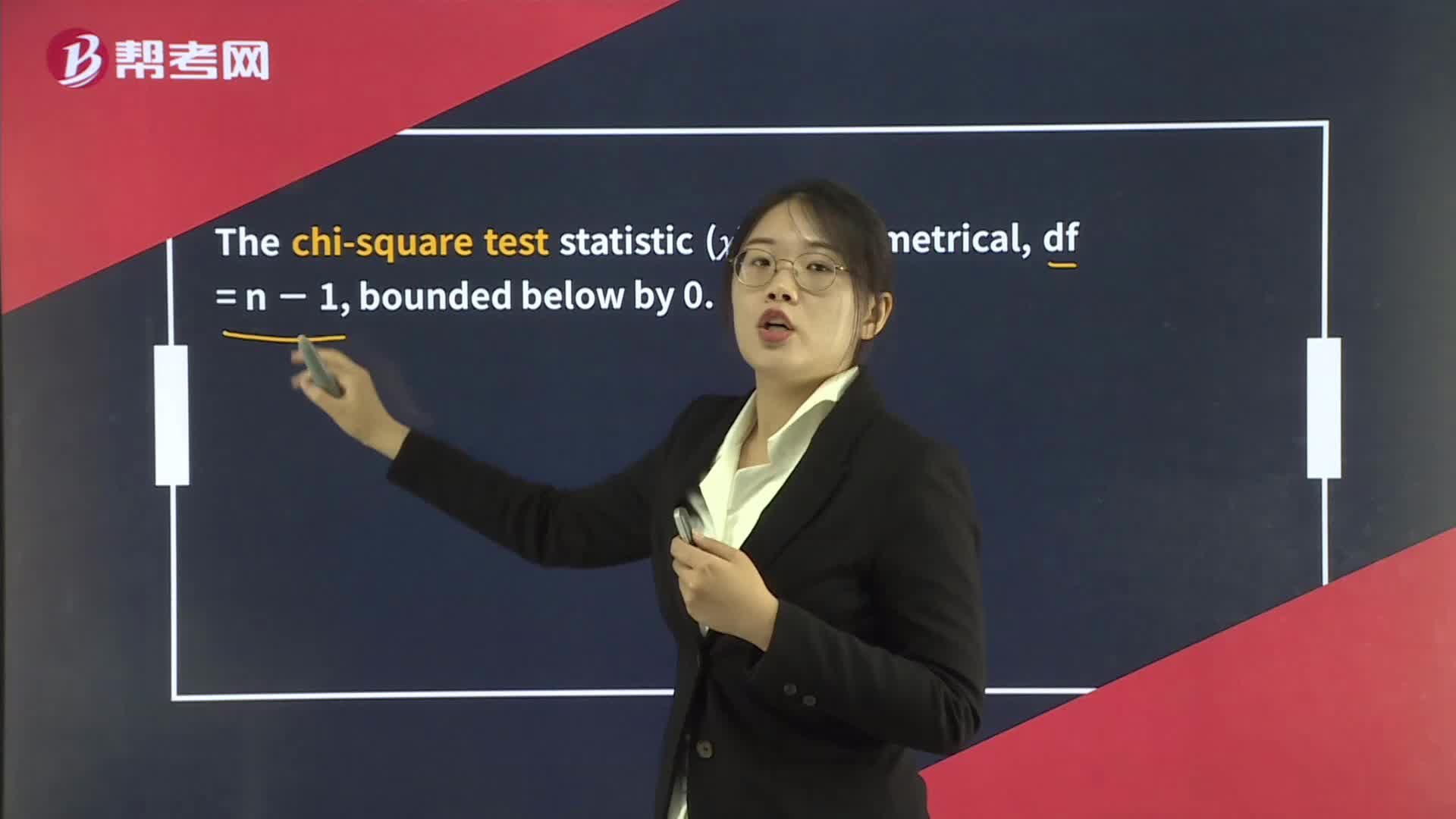

Hypothesis Tests Concerning Variance

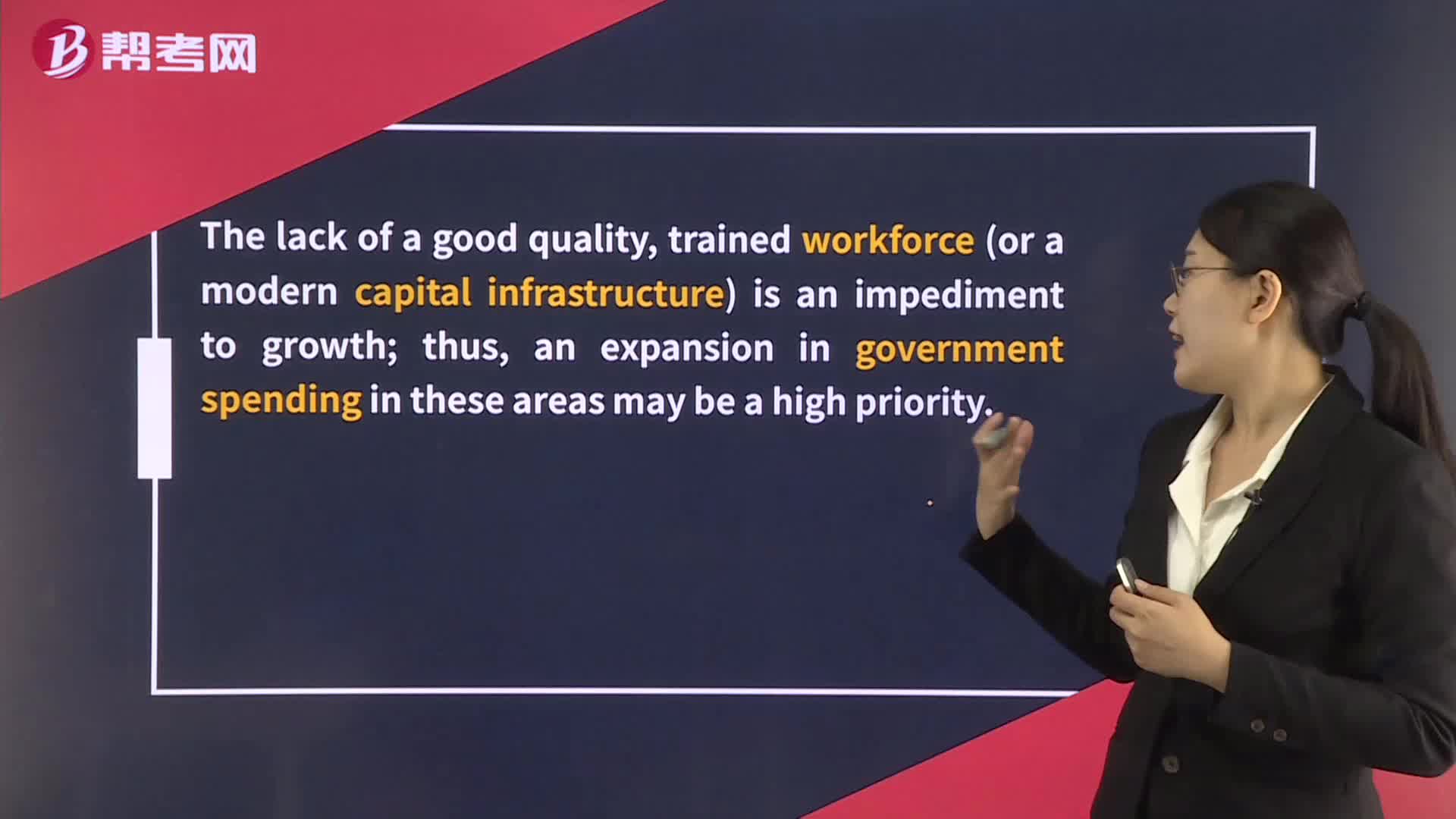

Benefits and Costs of Regional Trading Areas