CFA考試相關(guān)視頻

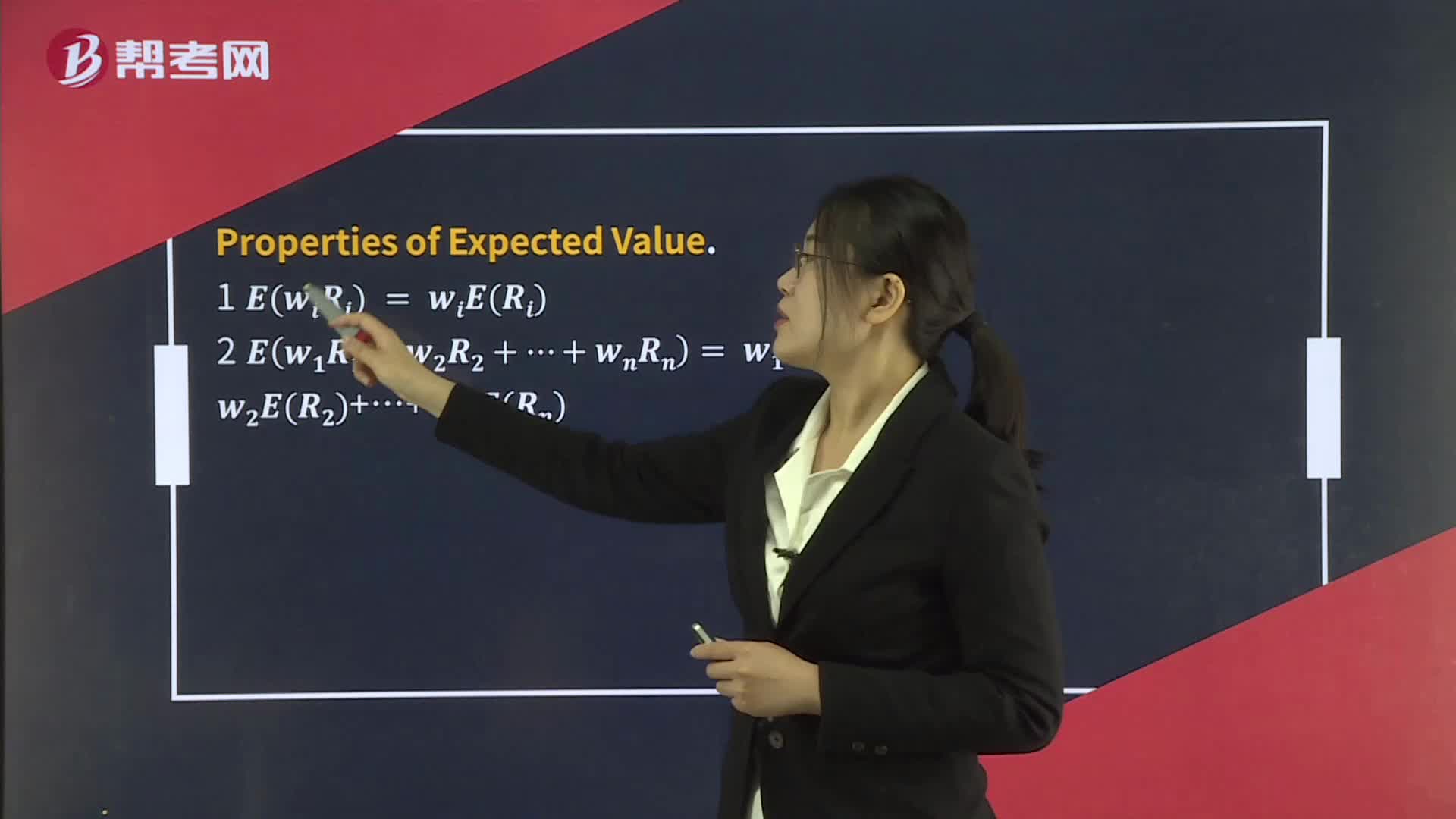

Portfolio Expected Return and Variance of Return

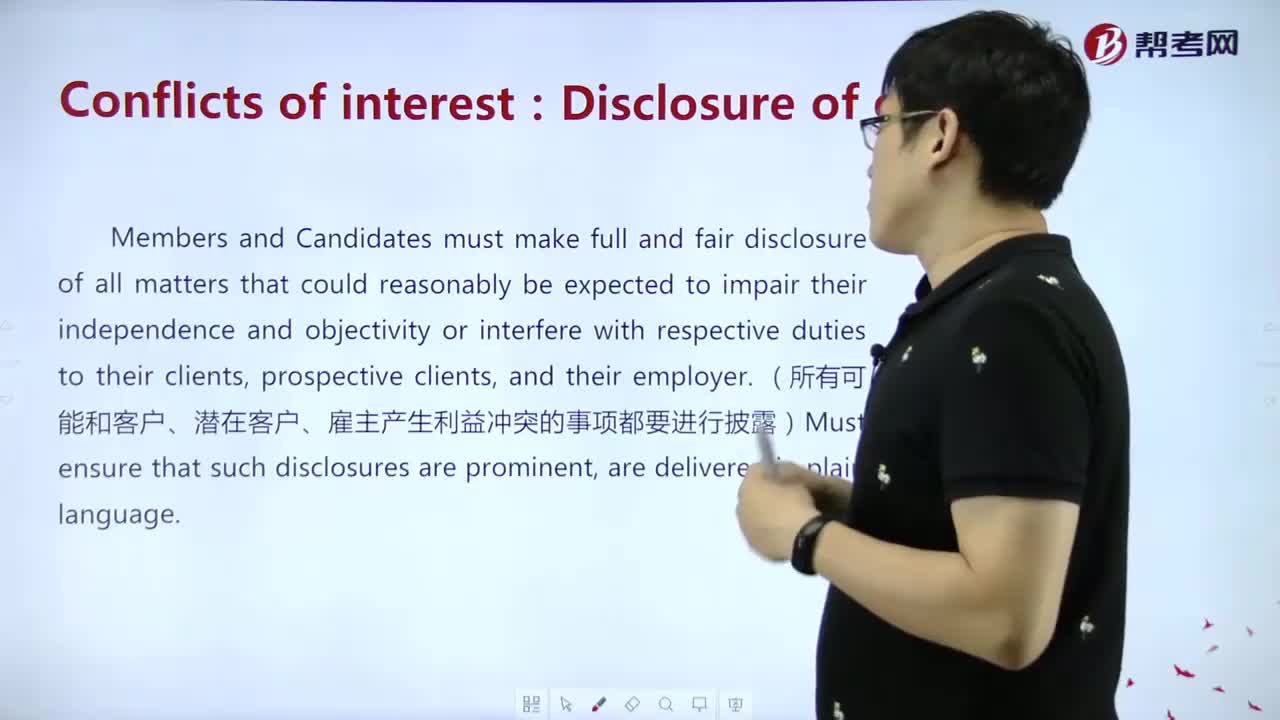

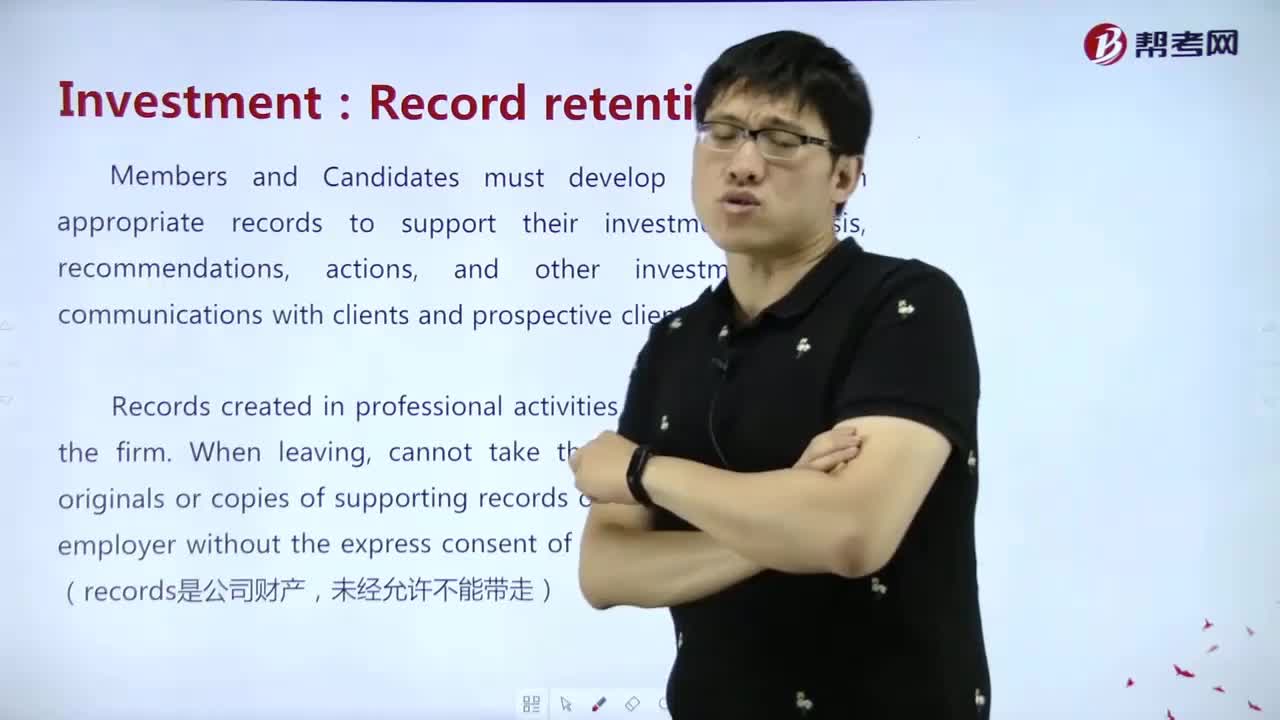

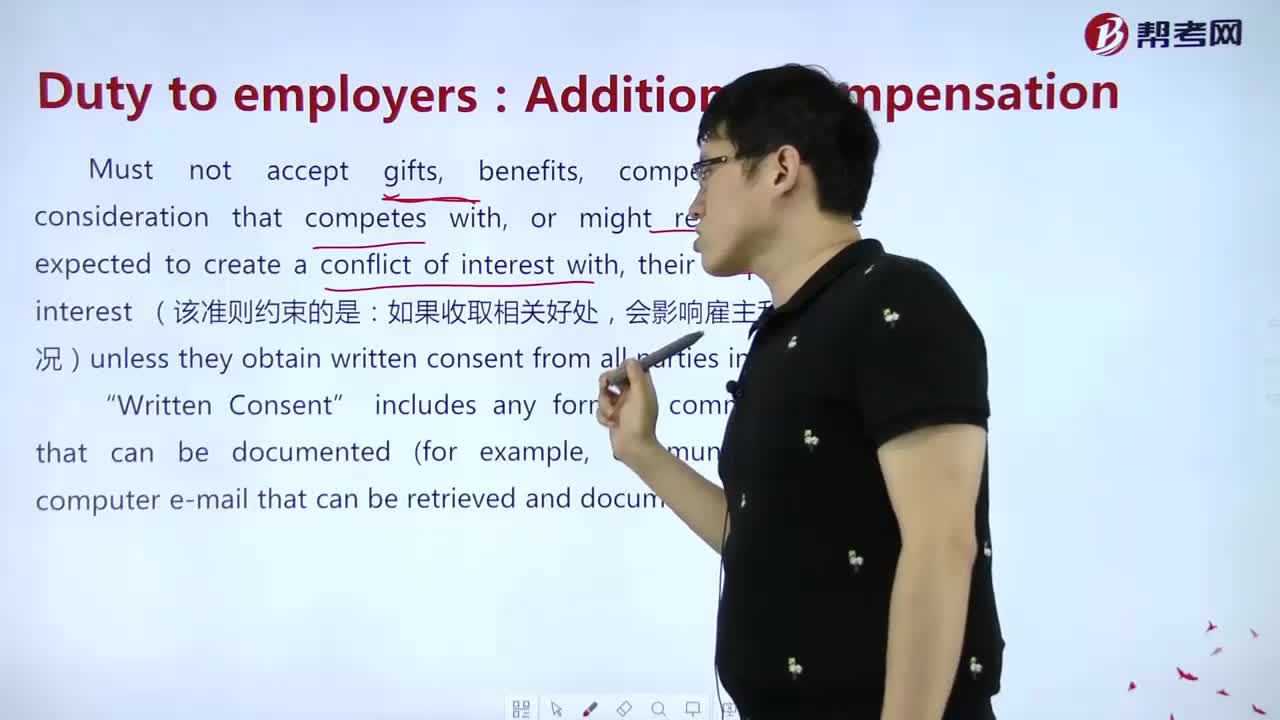

Limitations of Monetary Policy

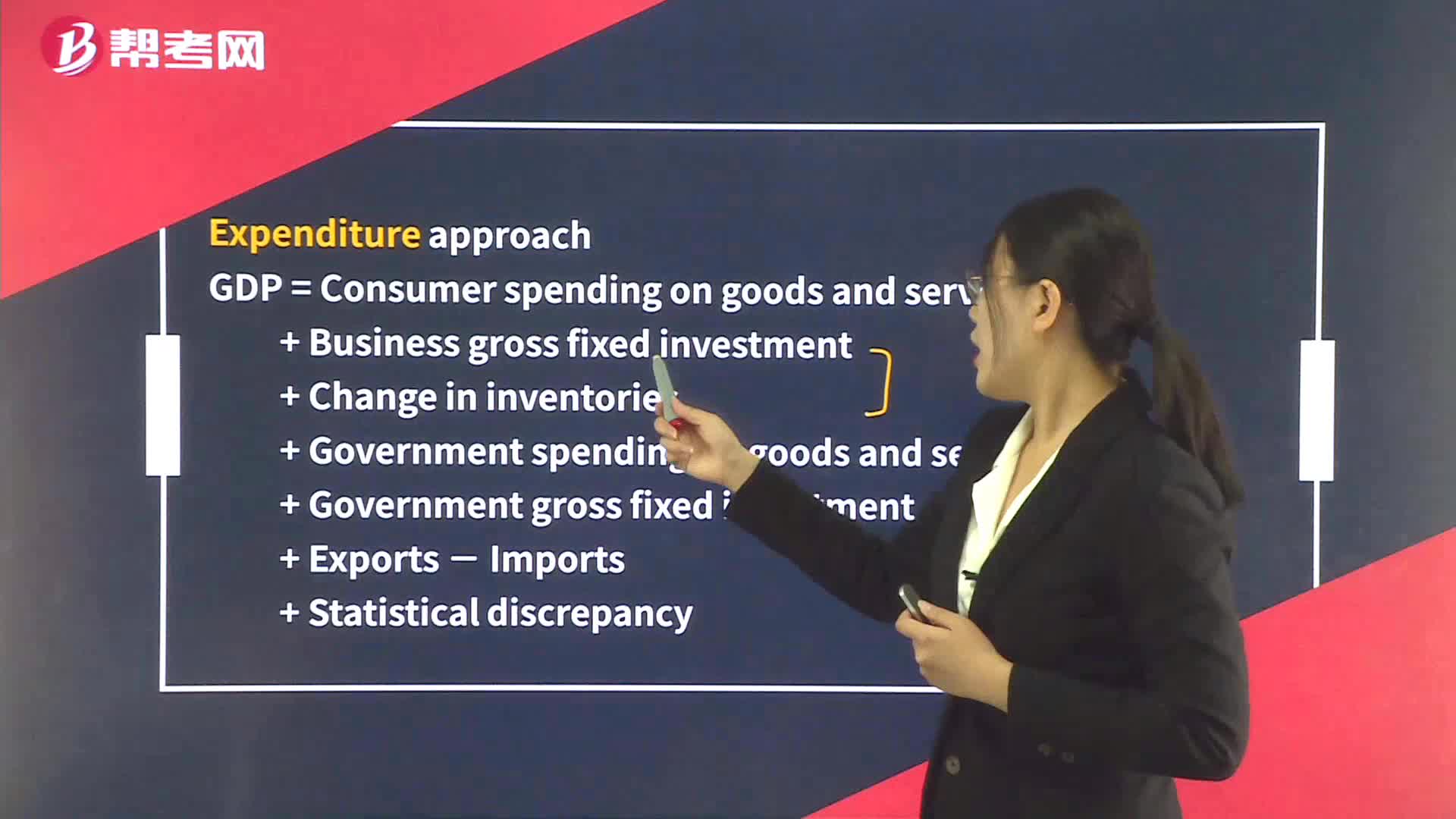

Calculation of GDP – Expenditure Approach

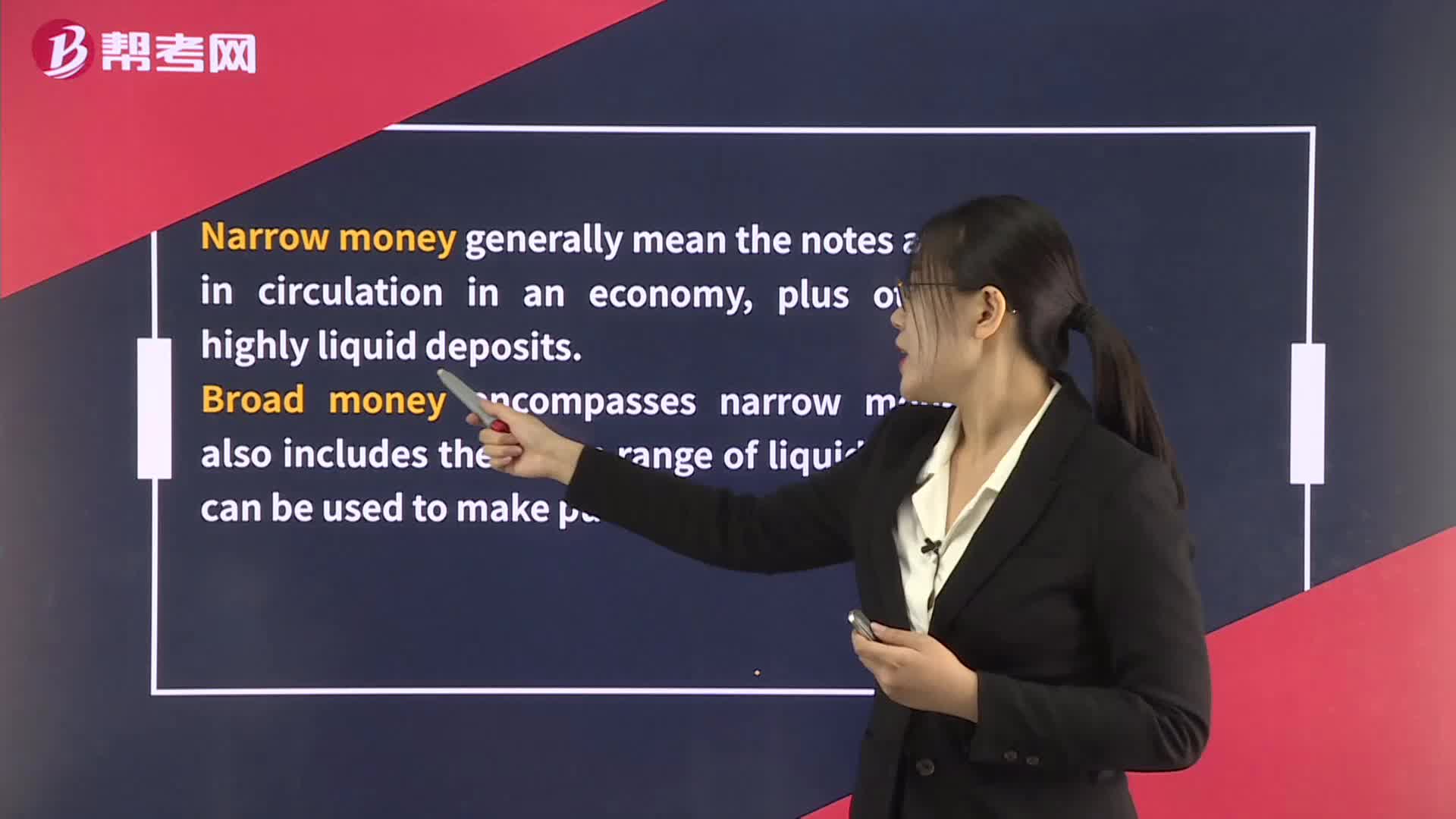

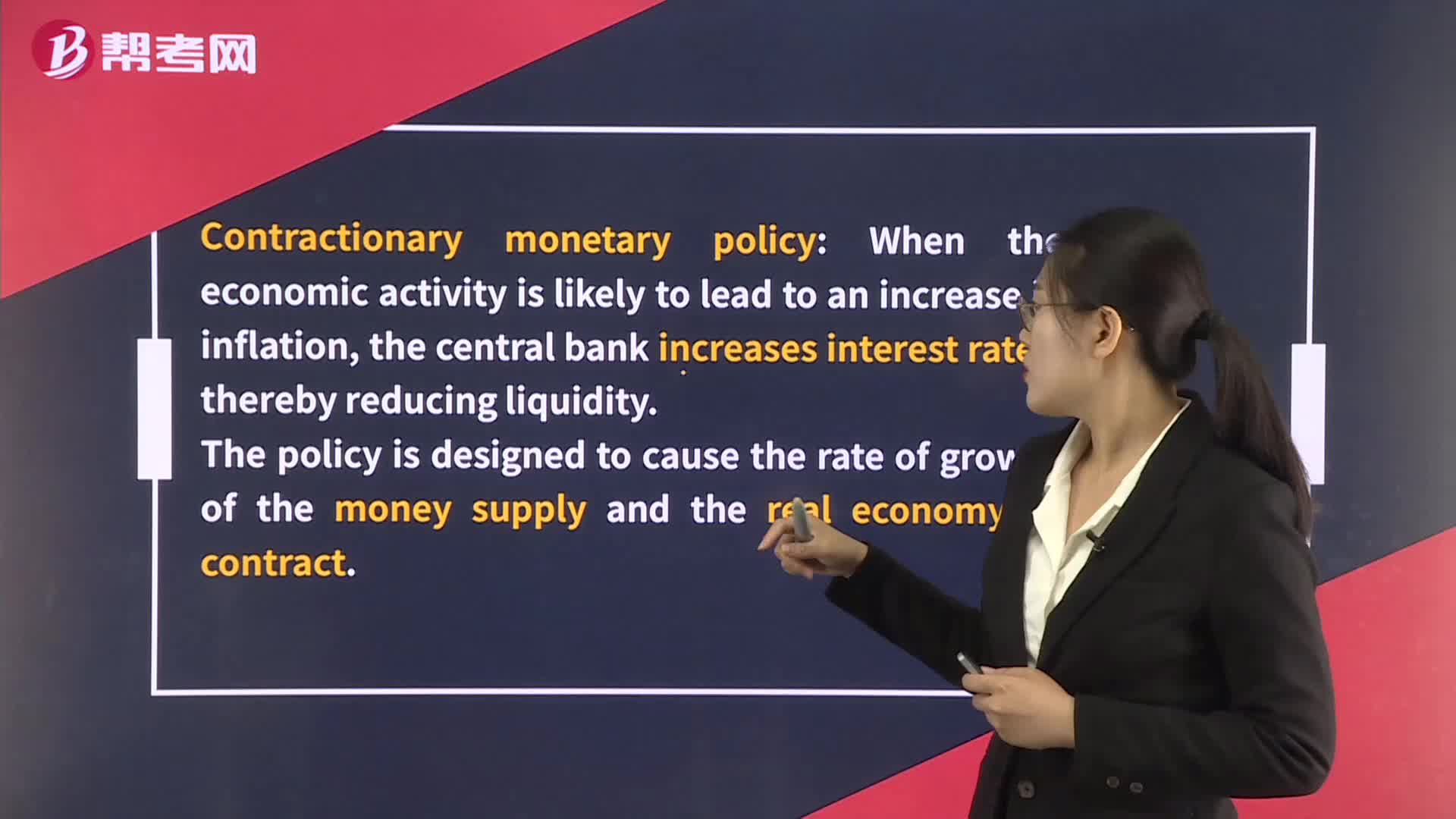

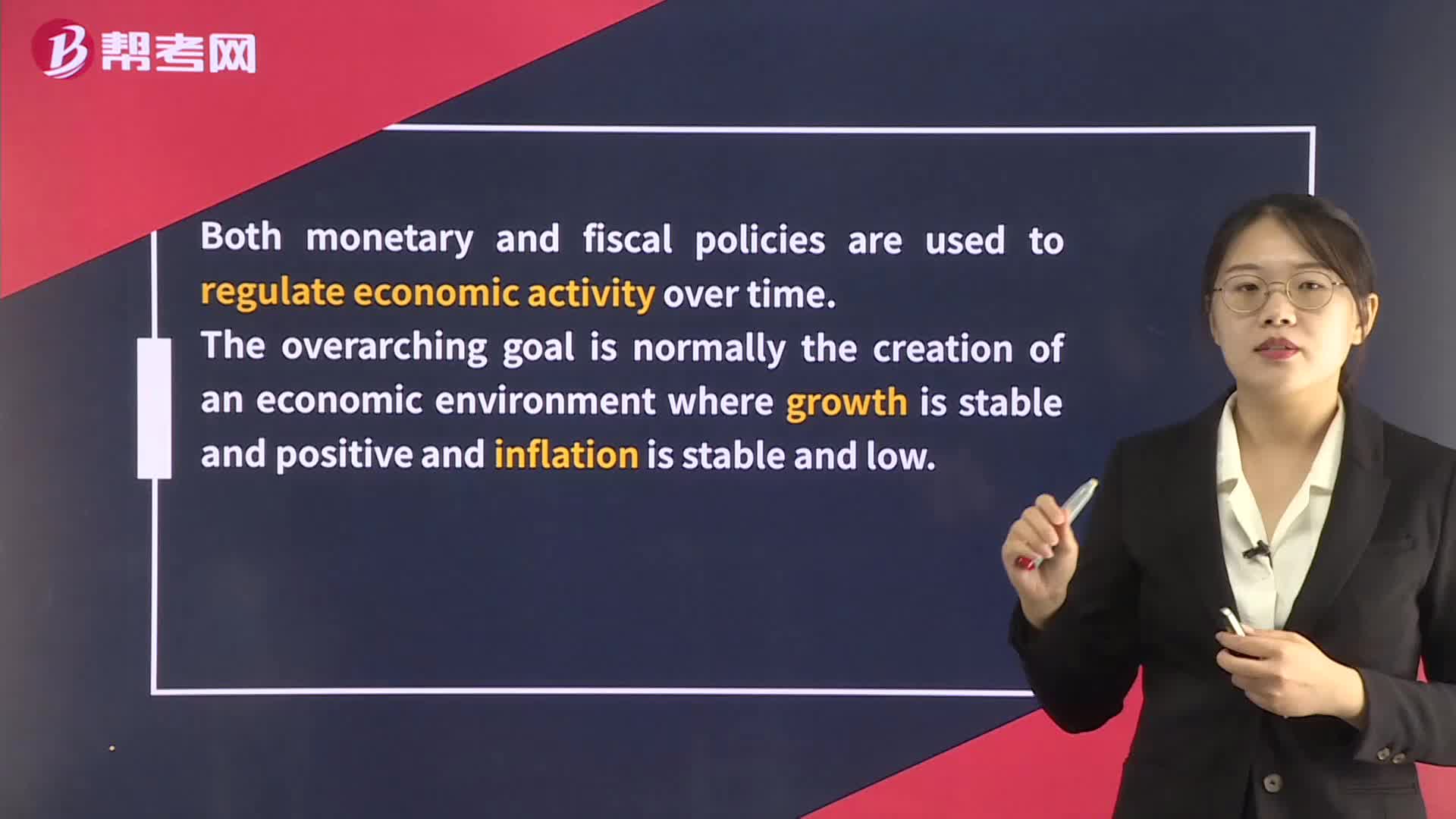

Monetary and Fiscal Policy

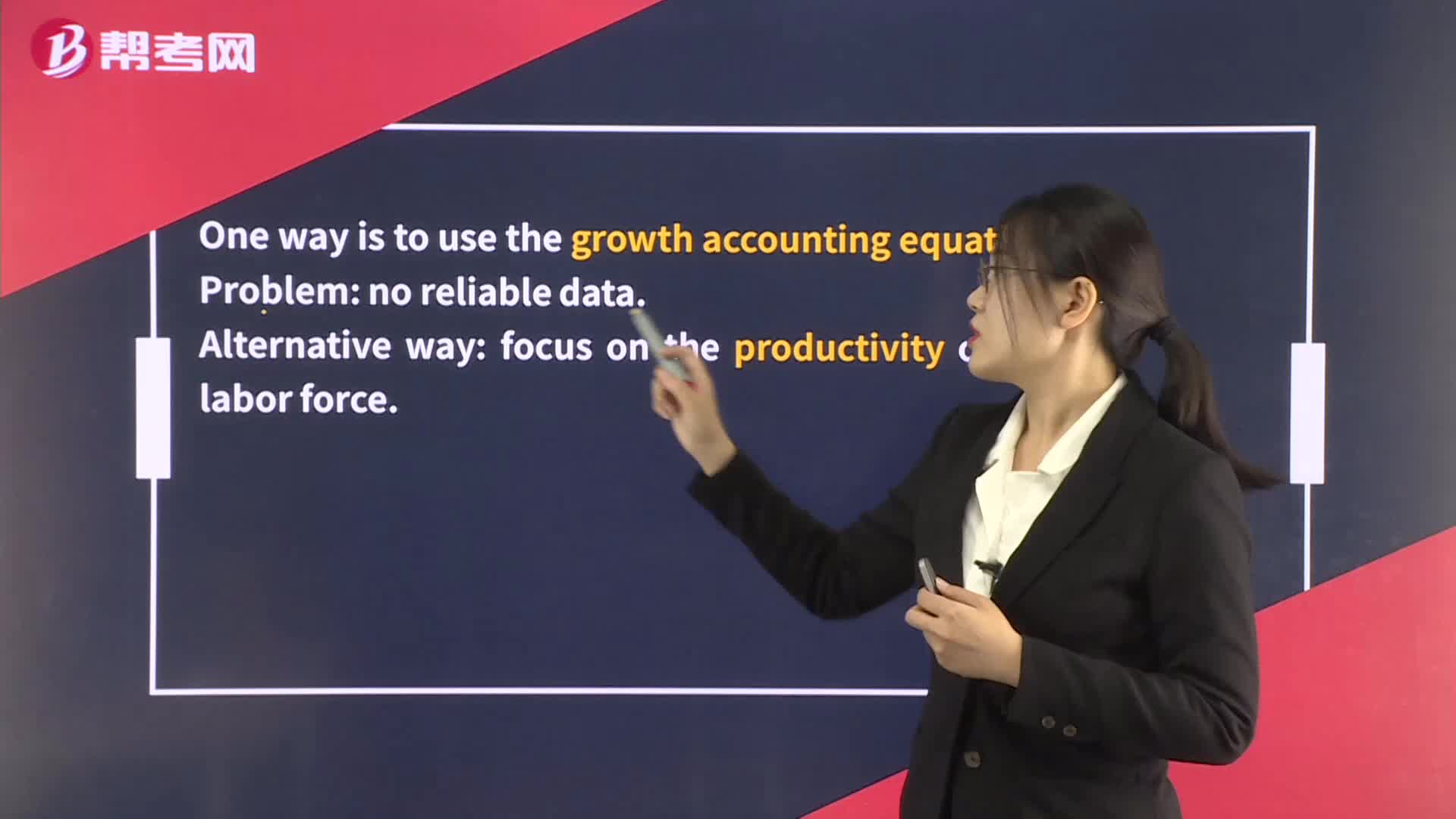

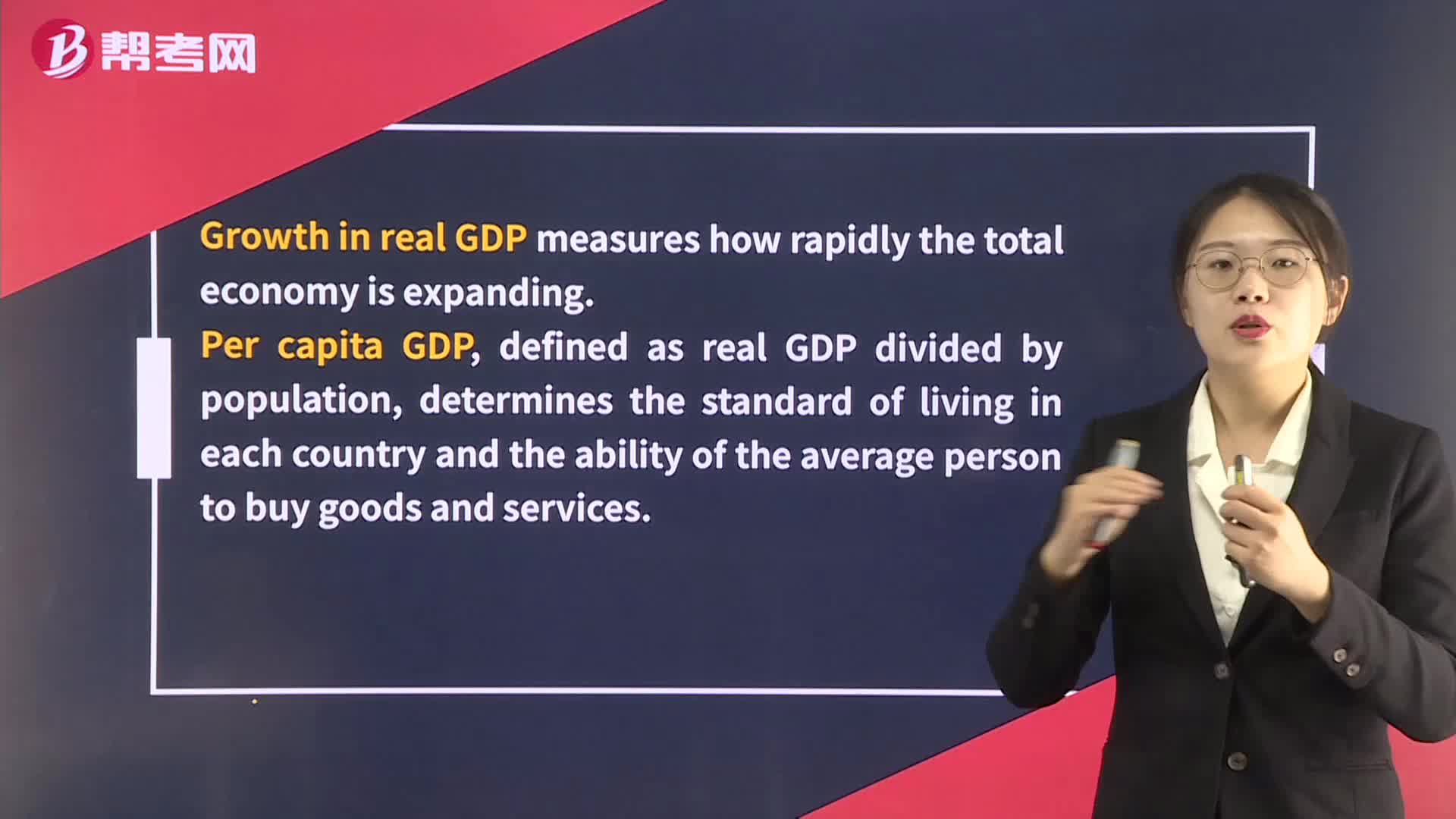

Economic Growth and Sustainability

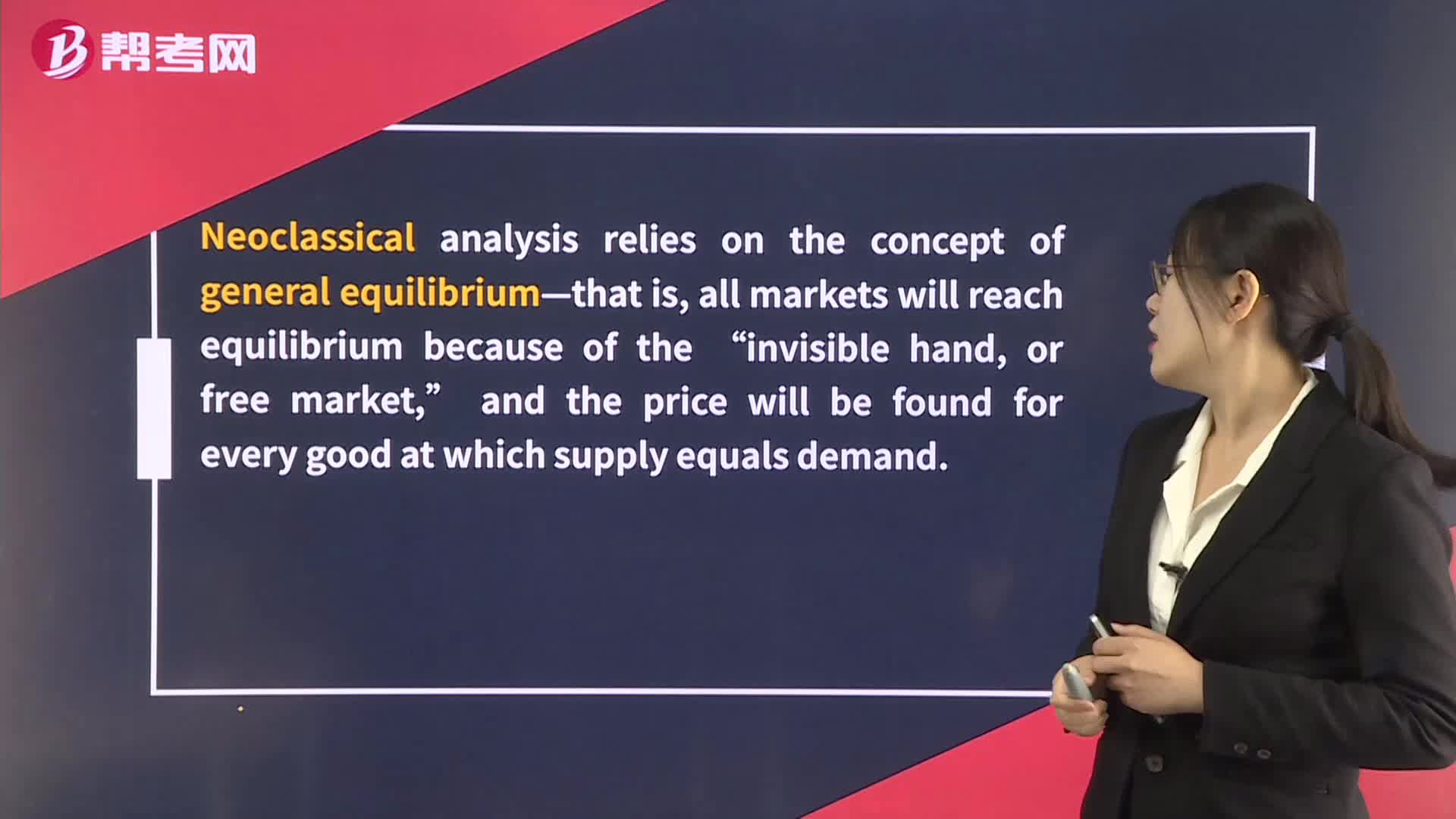

Theories of the Business Cycle - Neoclassical and Austrian Schools

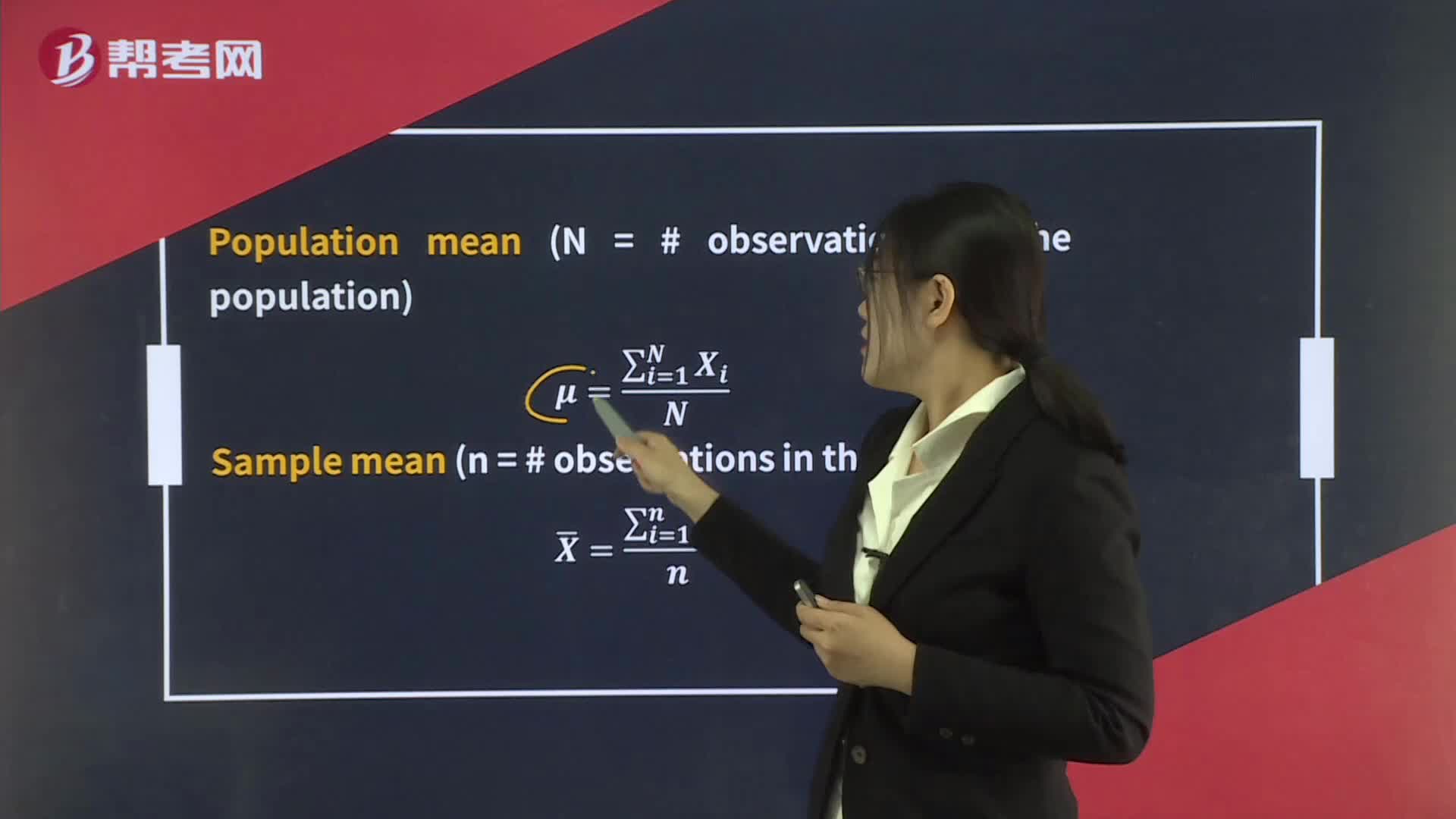

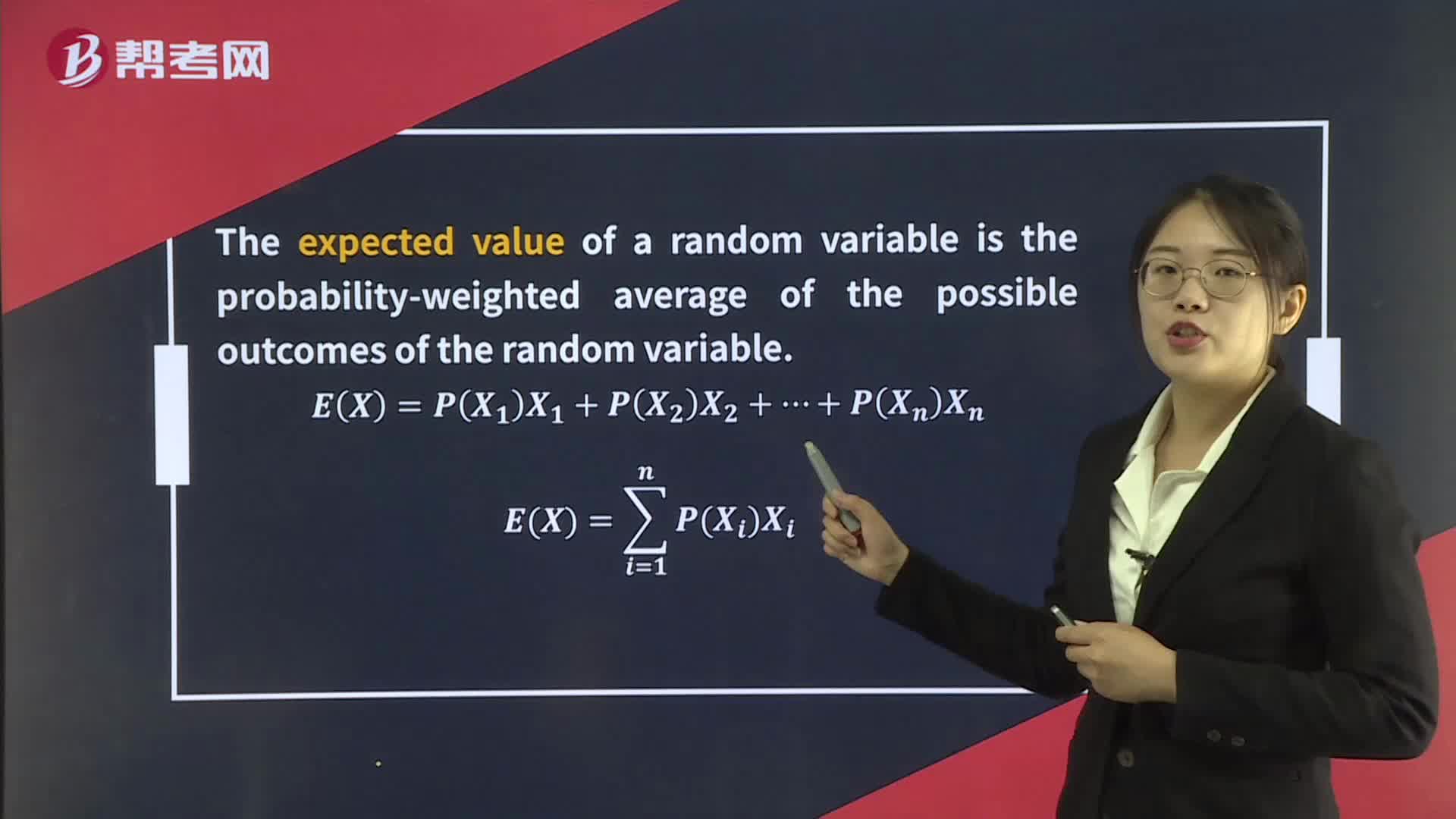

Expected Value & Variance

Theories of the Business Cycle - Keynesian School

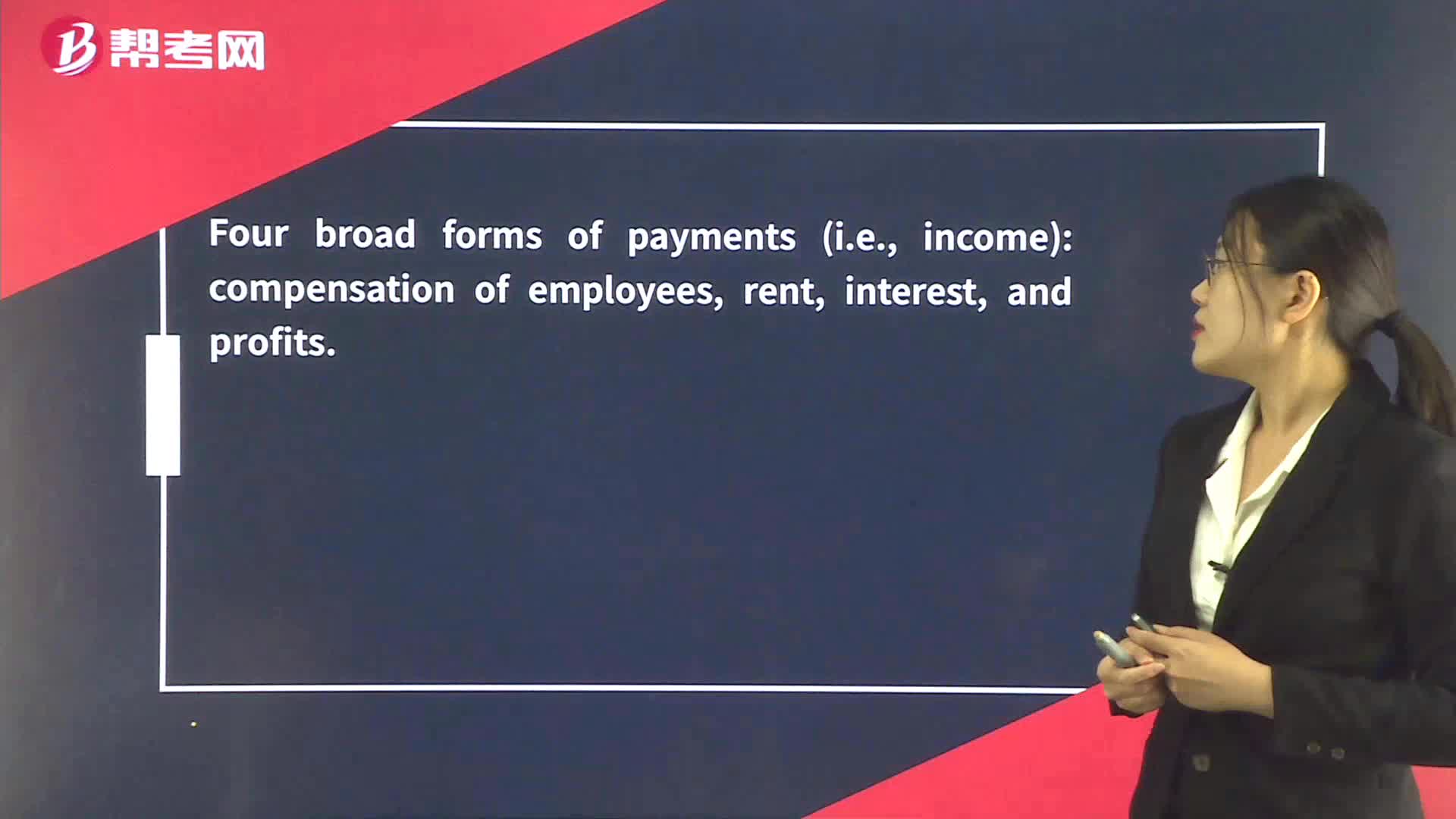

Aggregate Output and Income

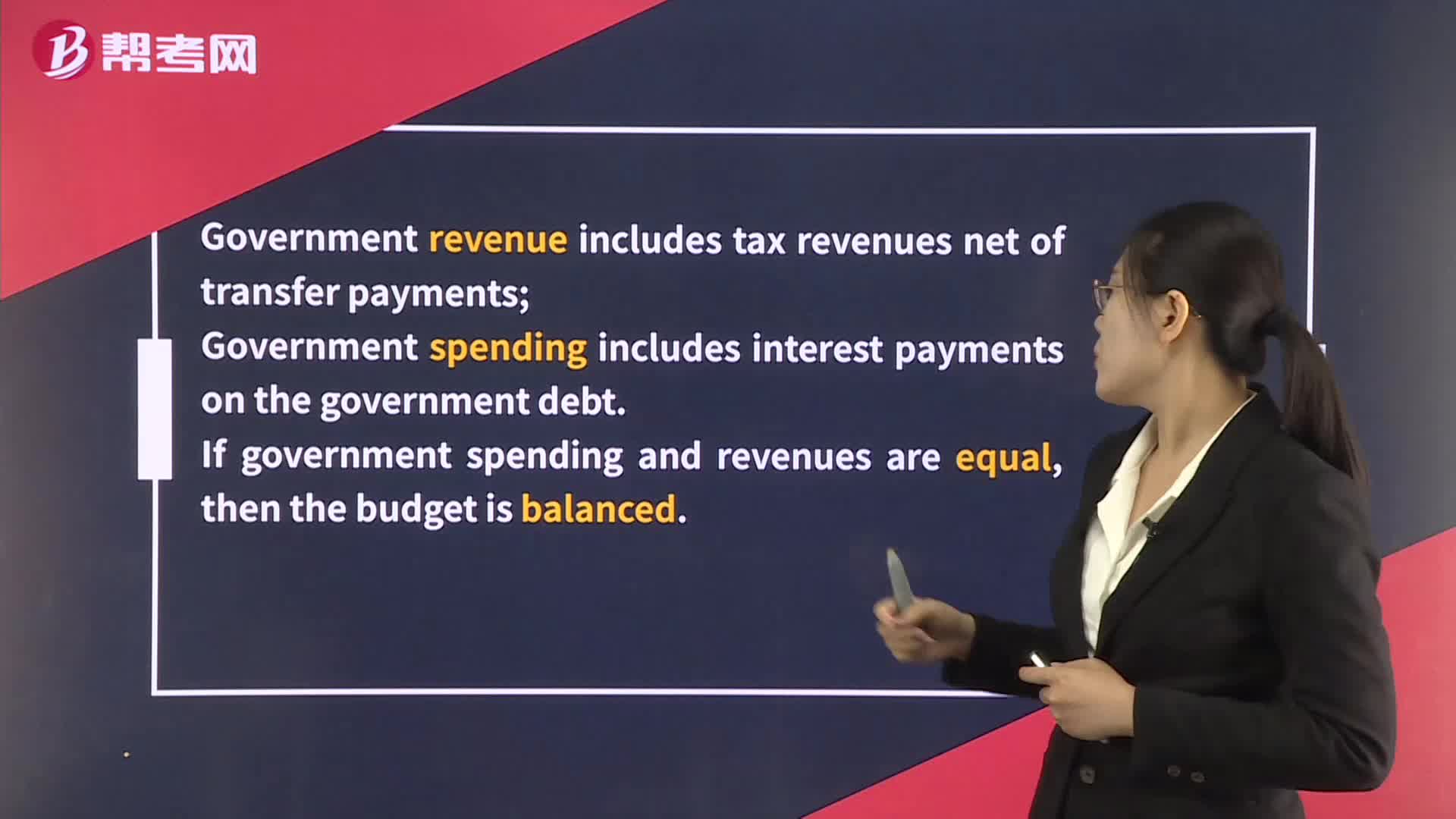

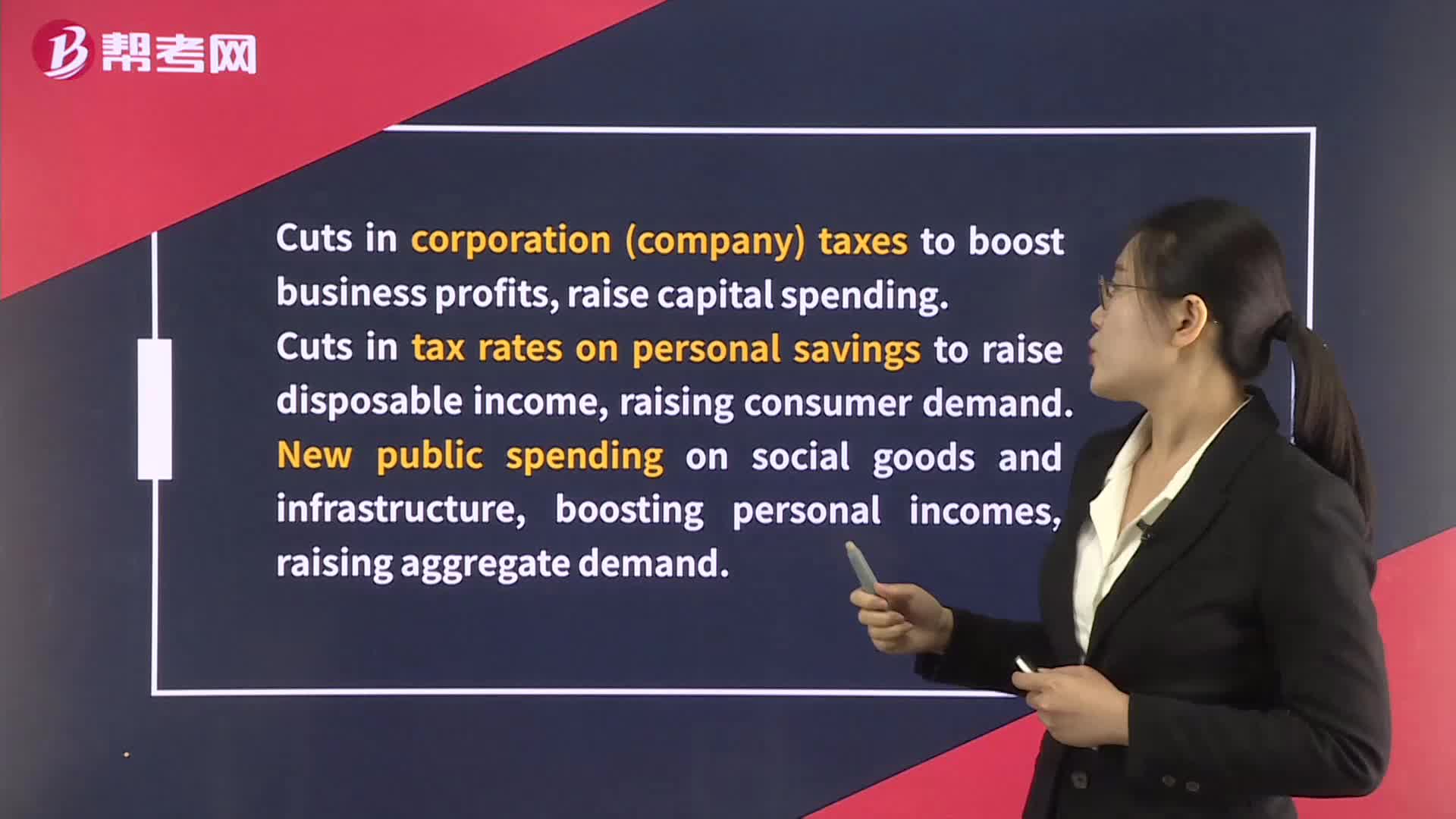

Fiscal Policy and Aggregate Demand

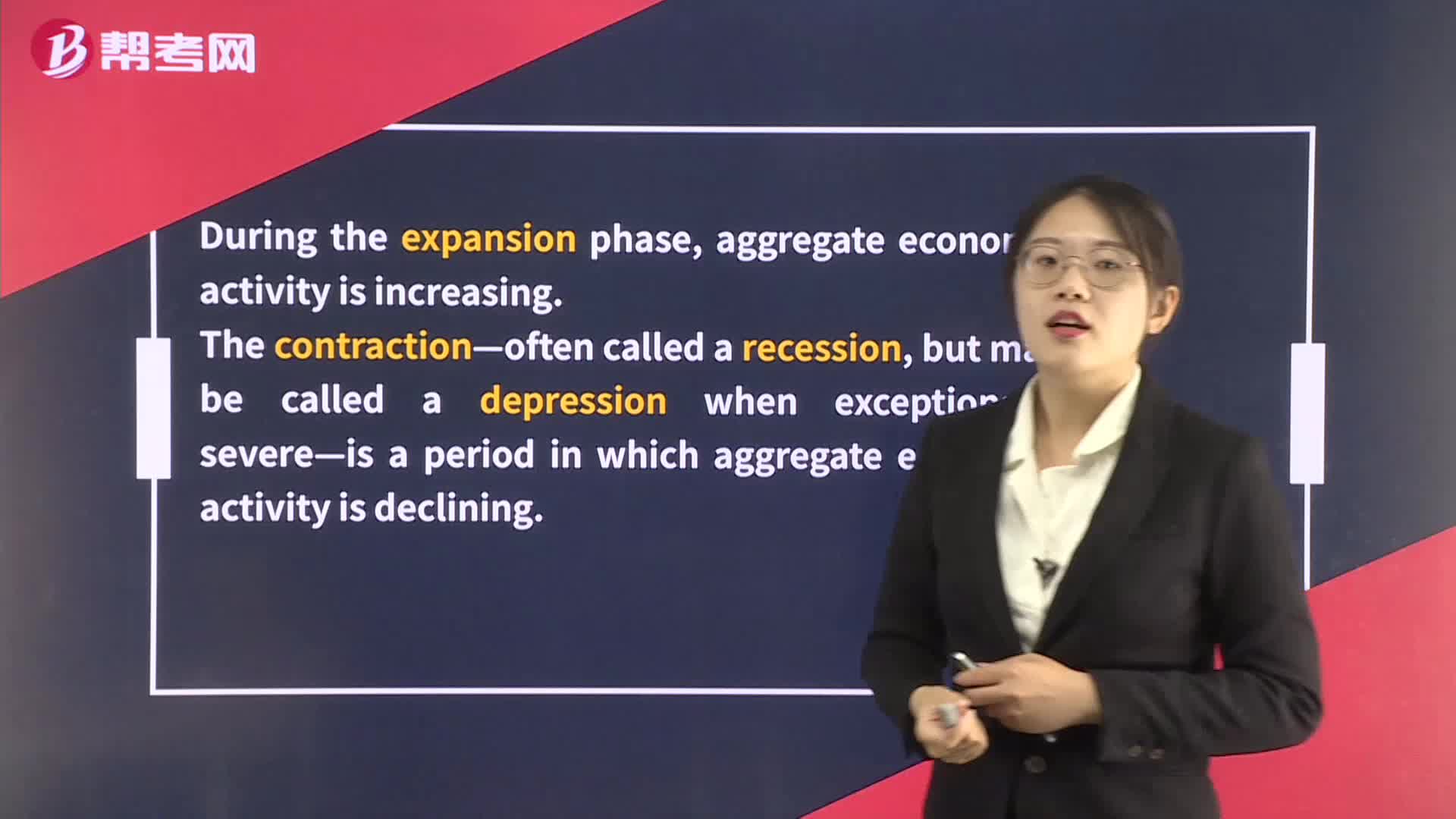

Phases Of the Business Cycle

Deflation, Hyperinflation, and Disinflation