CFA考試相關(guān)視頻

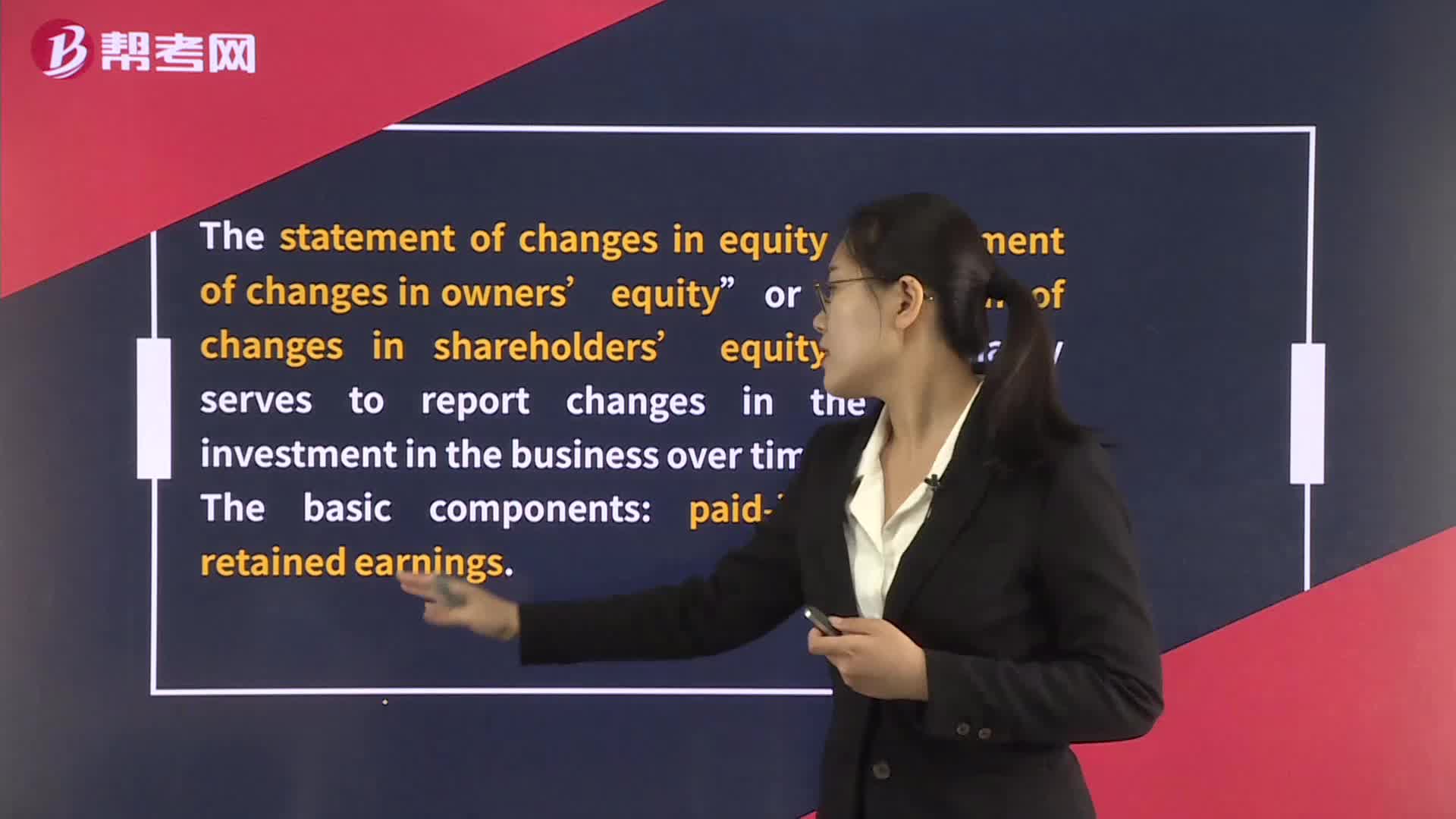

Statement of Changes in Equity

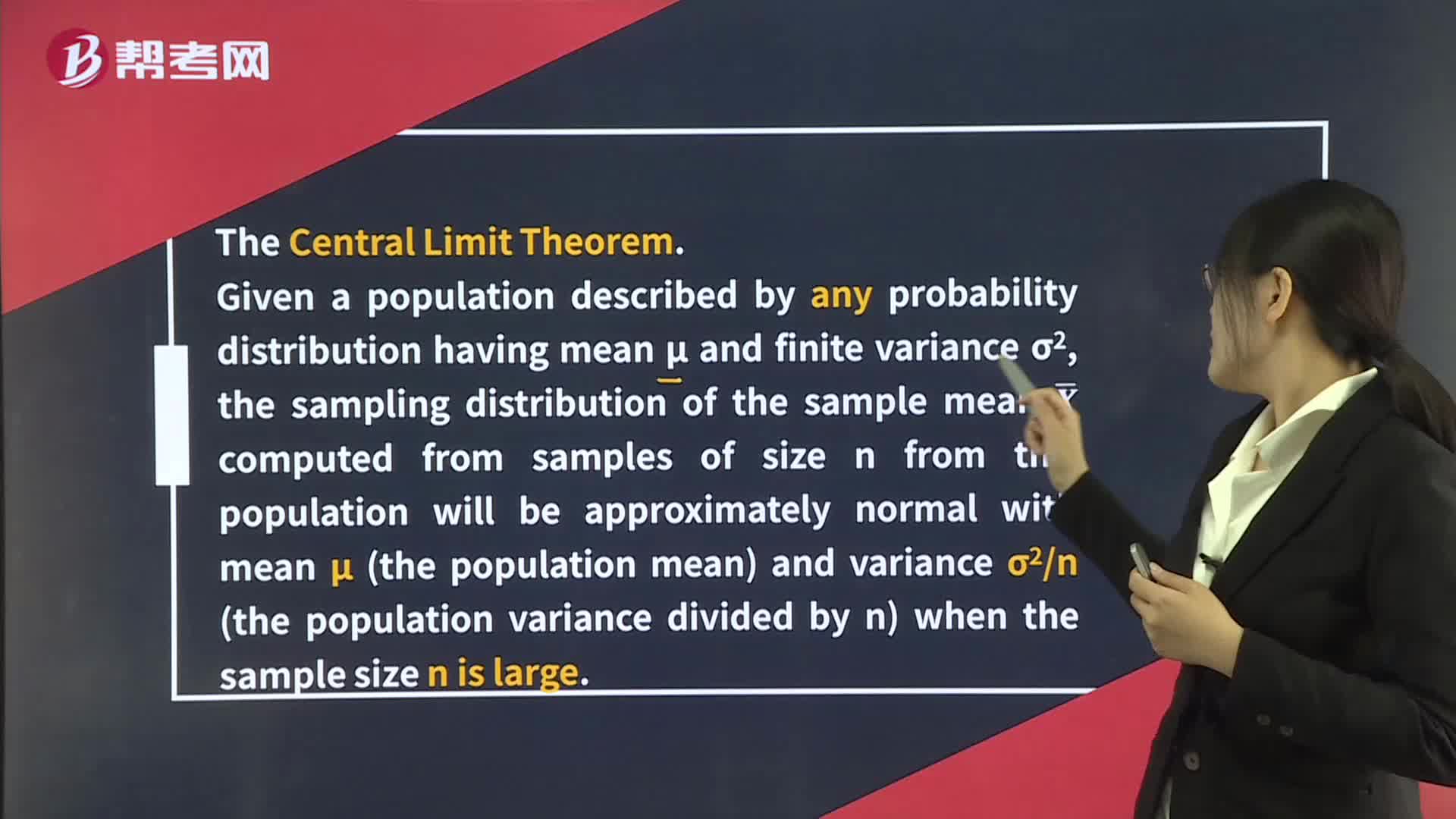

Distribution of the Sample Mean

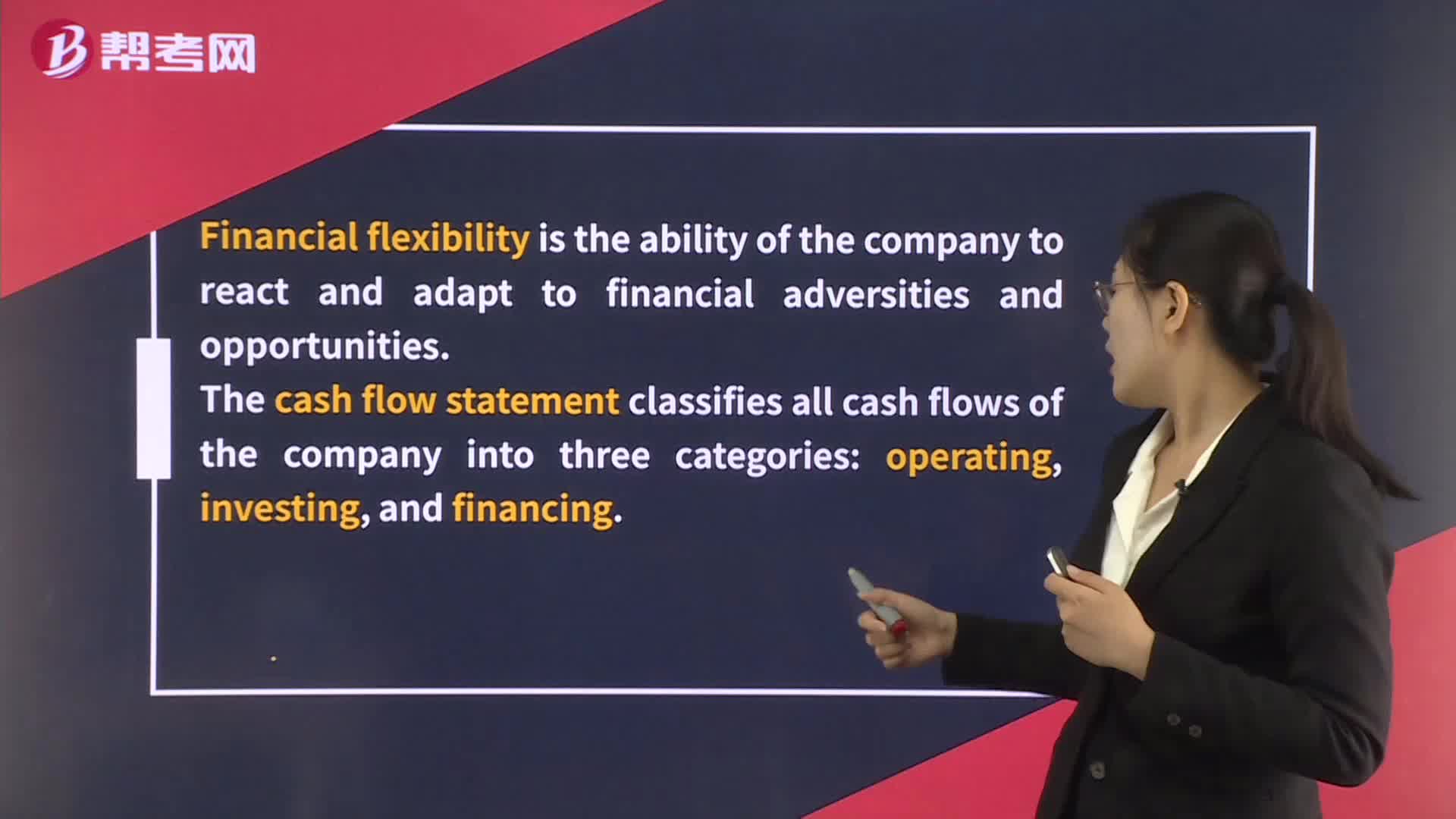

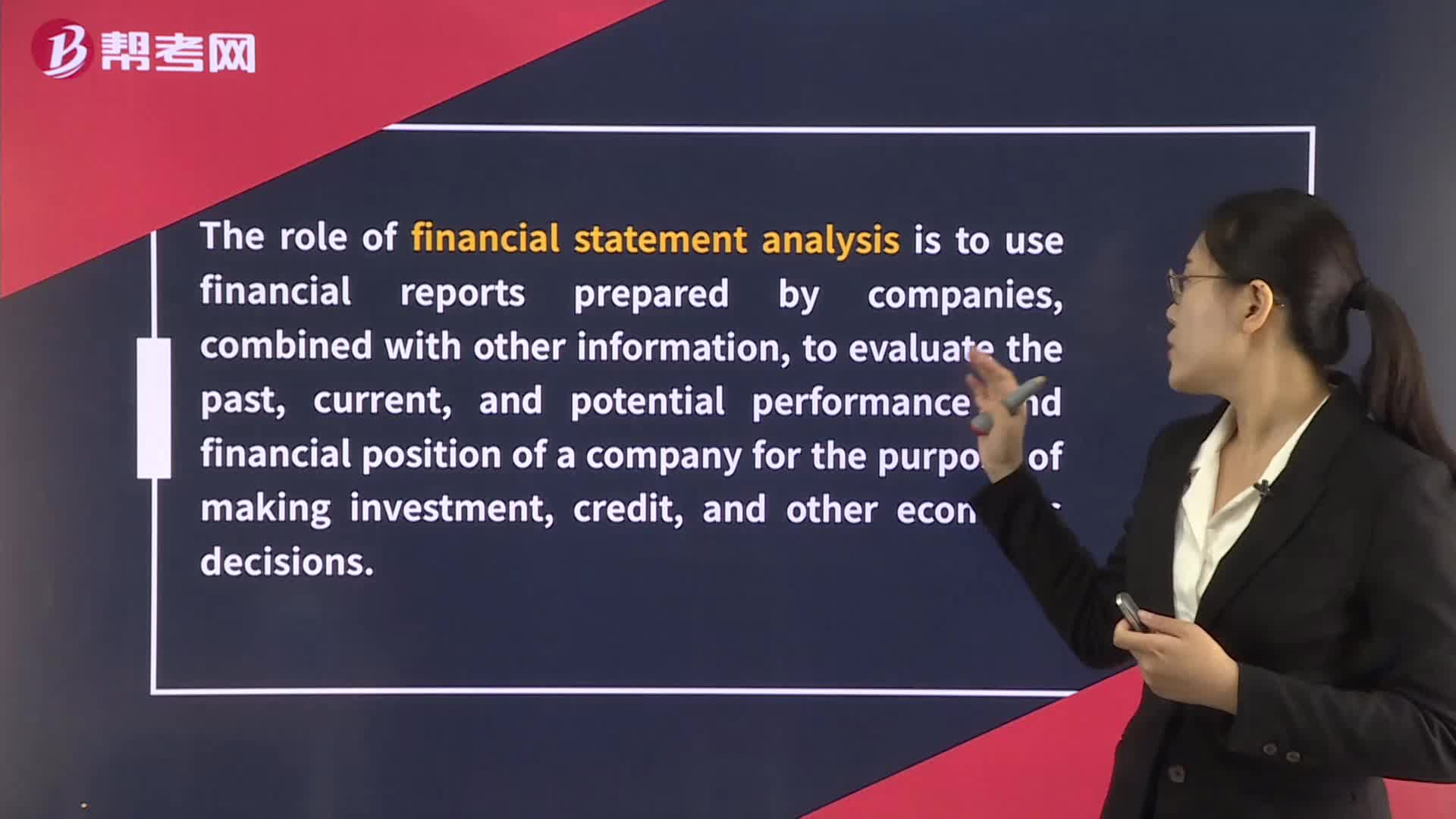

Scope of Financial Statement Analysis

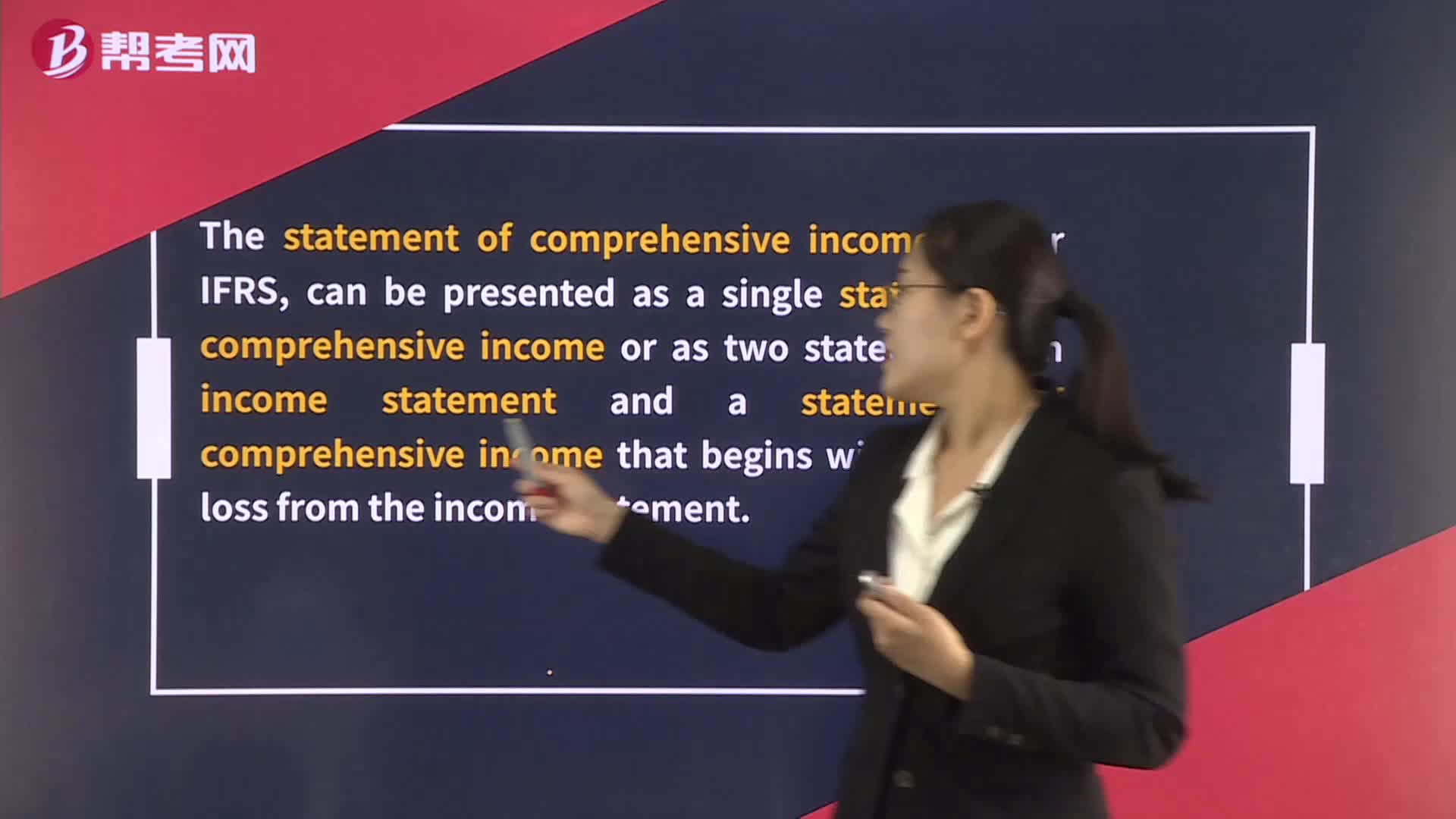

Statement of Comprehensive Income

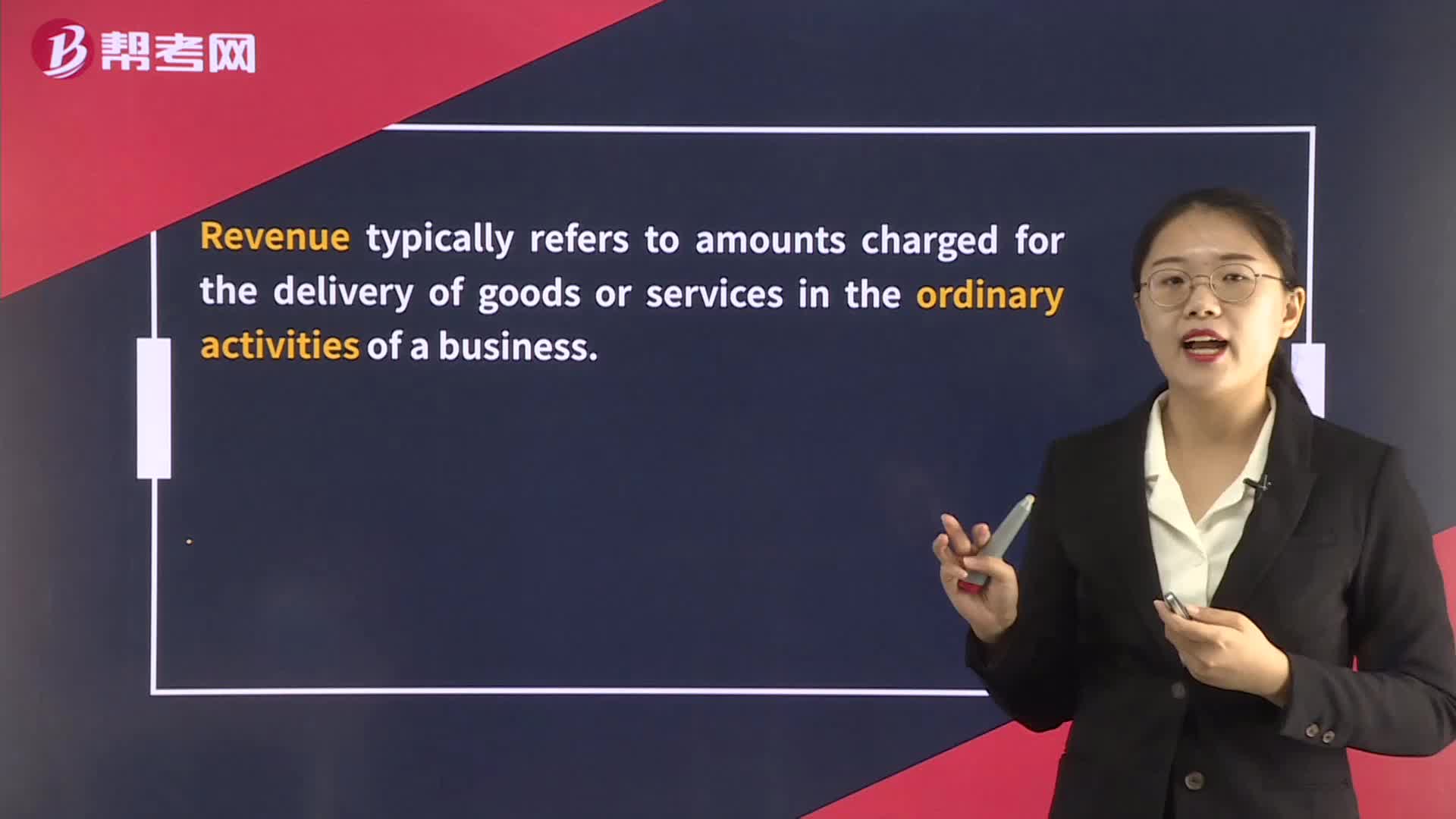

Income Statement – Revenue, Other Income, Expenses

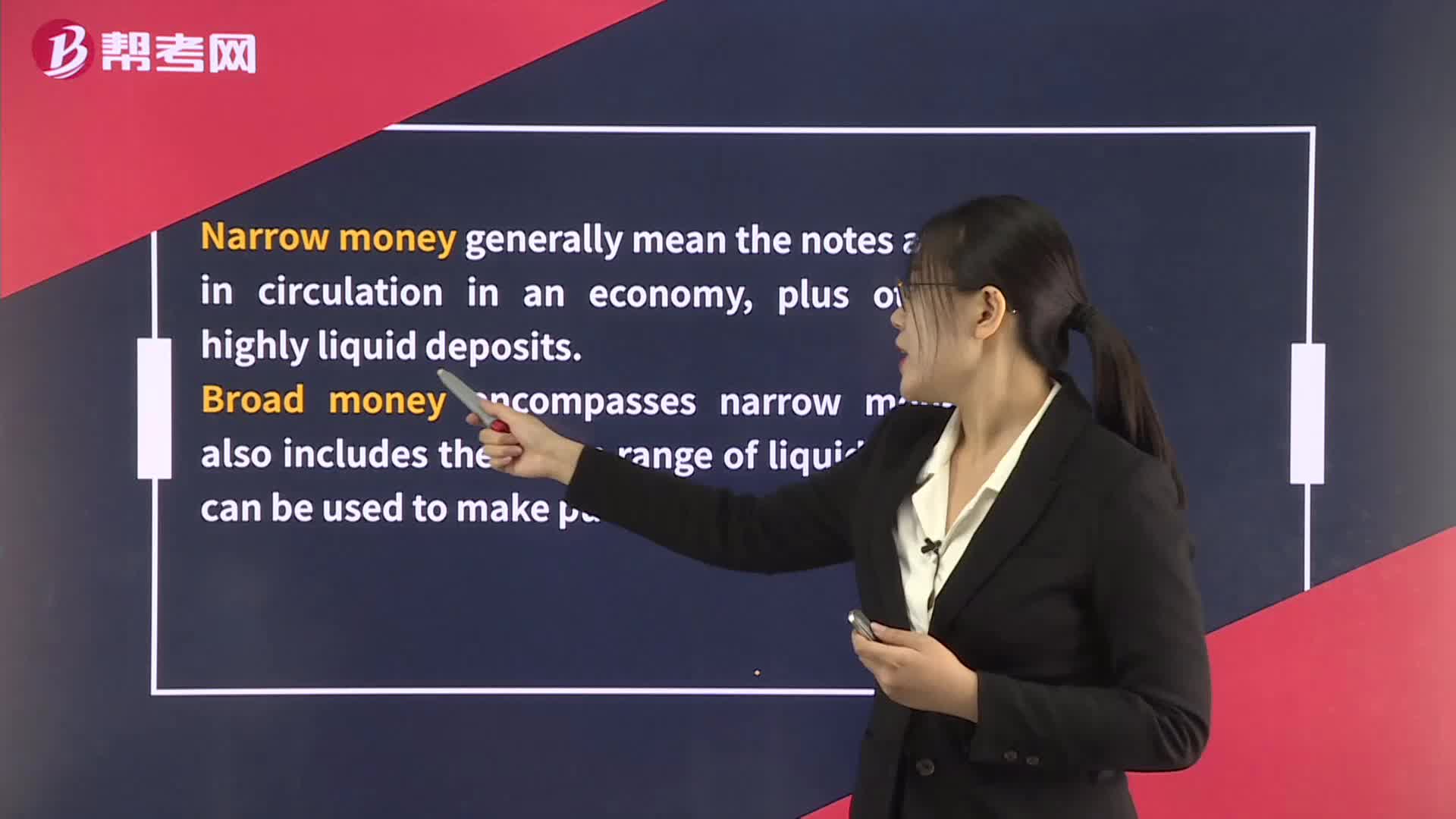

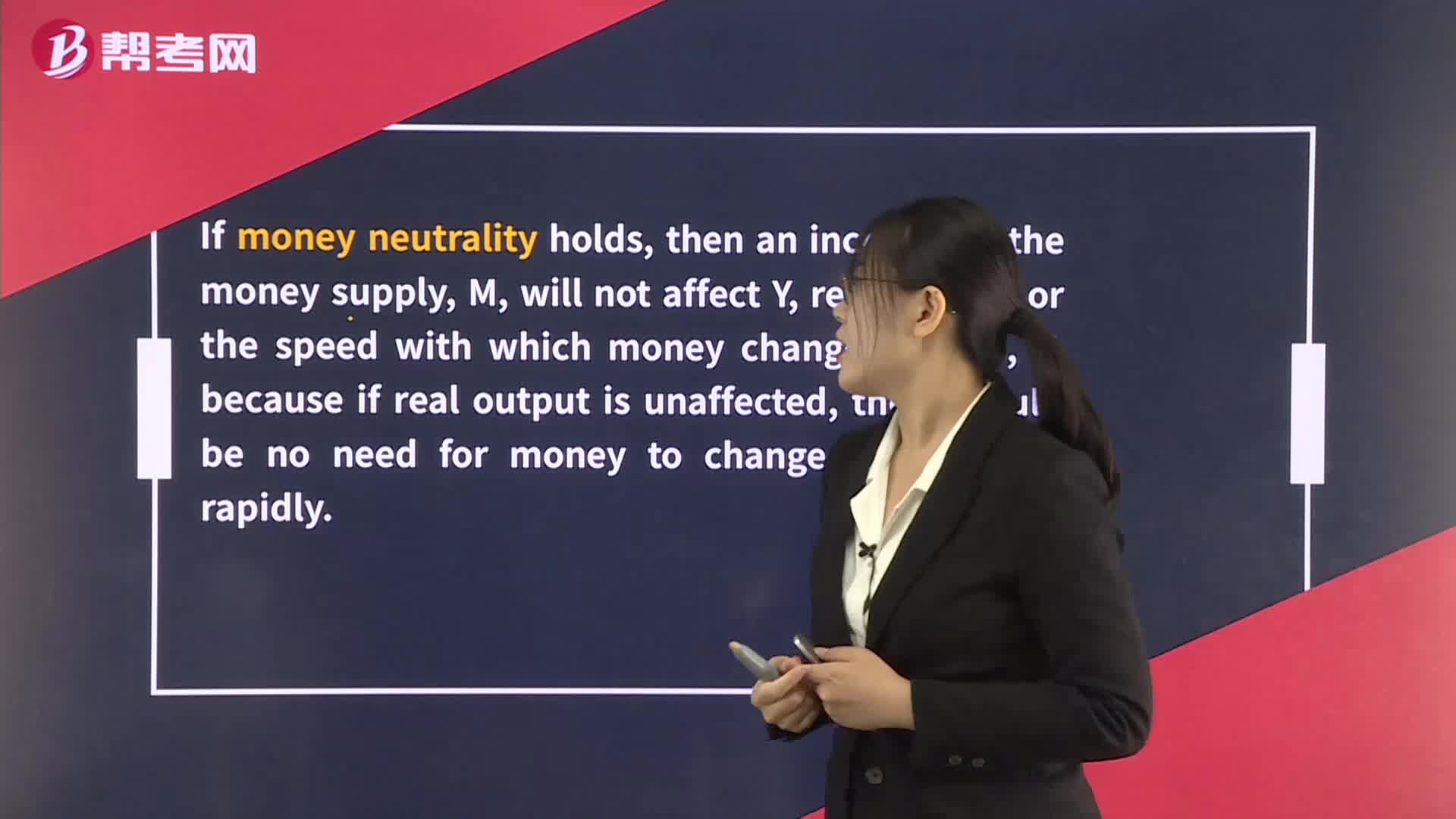

The Quantity Theory of Money

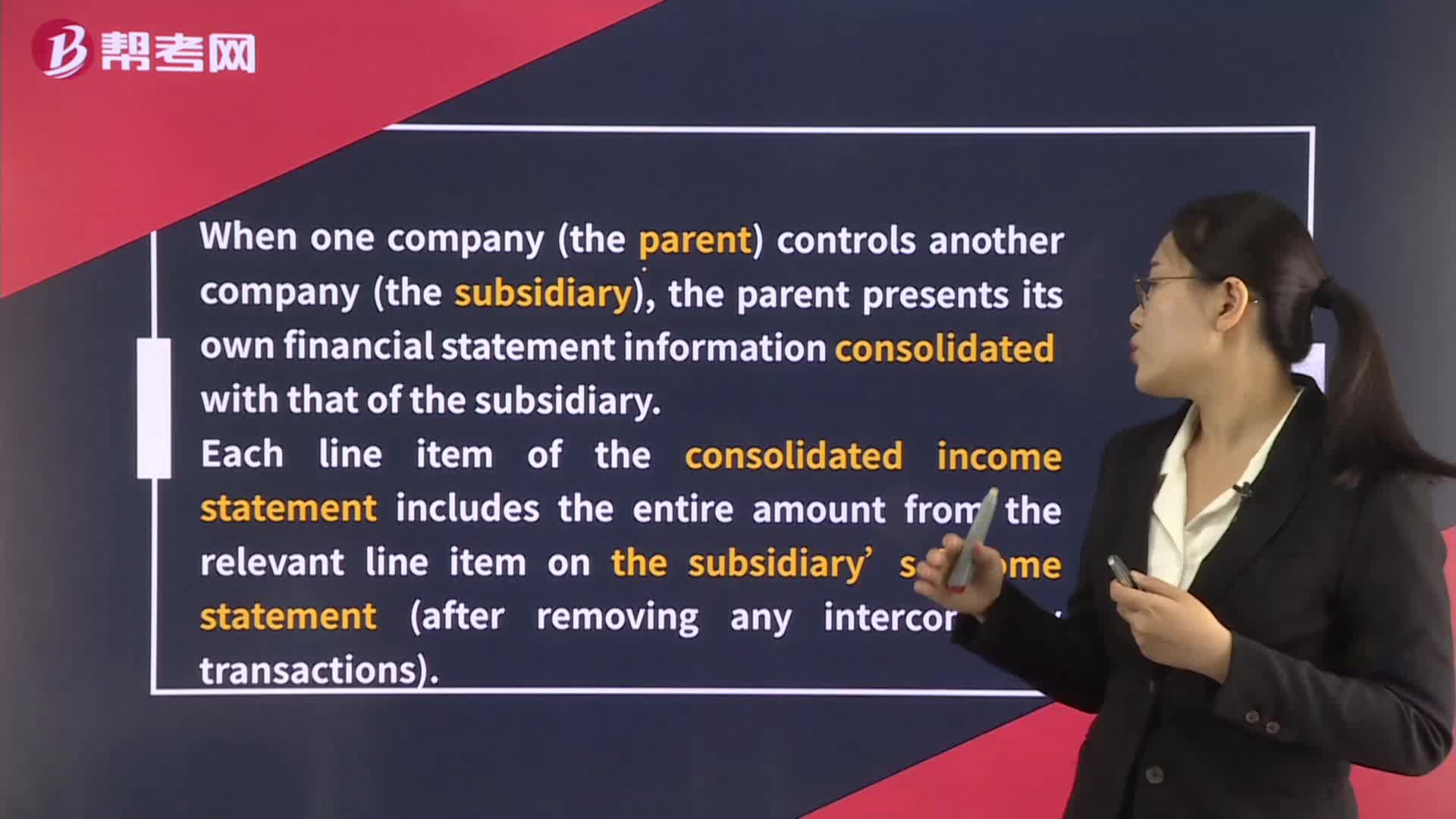

Income Statement– Minority Interest

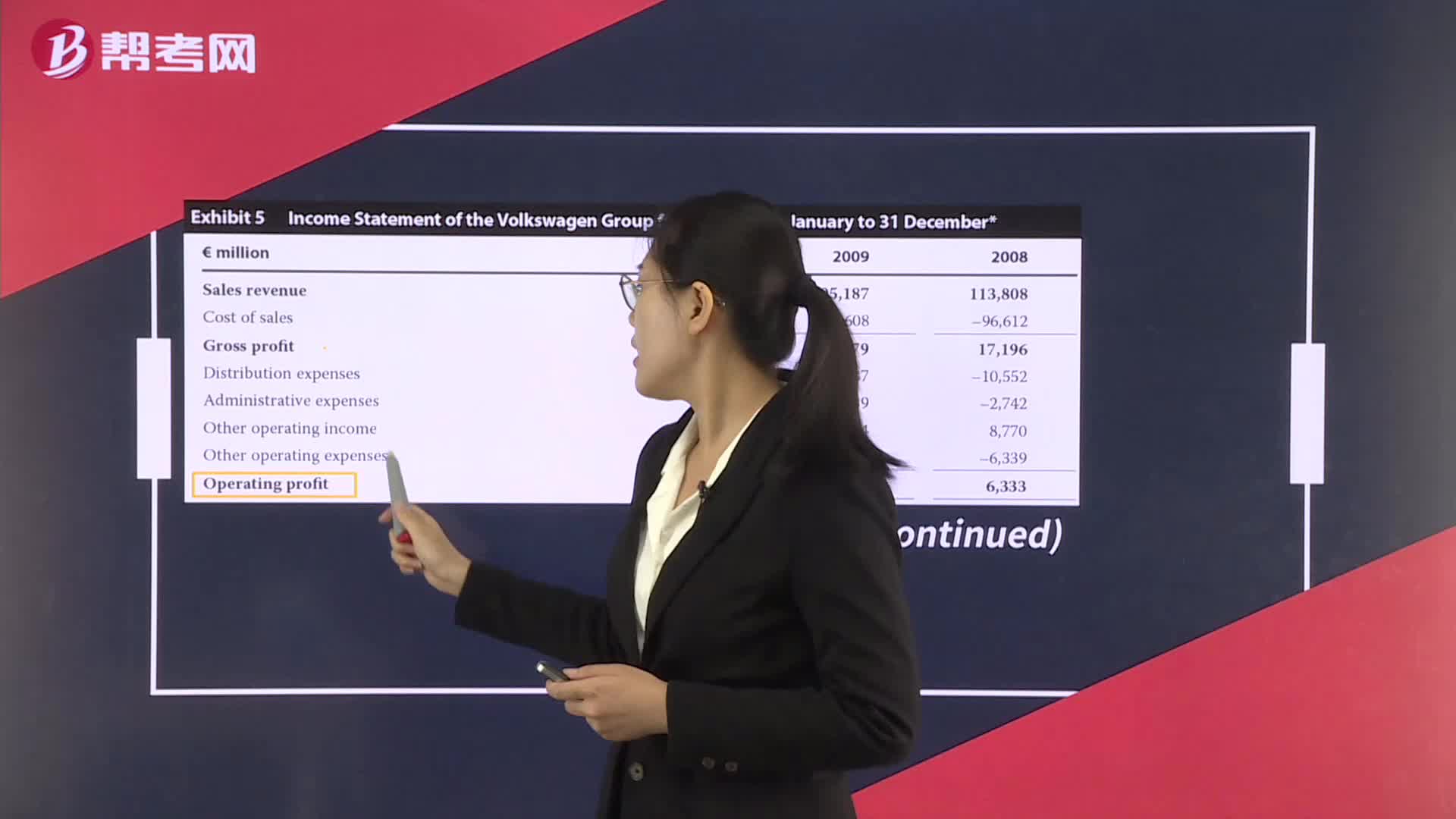

Income Statement– Operating Profit

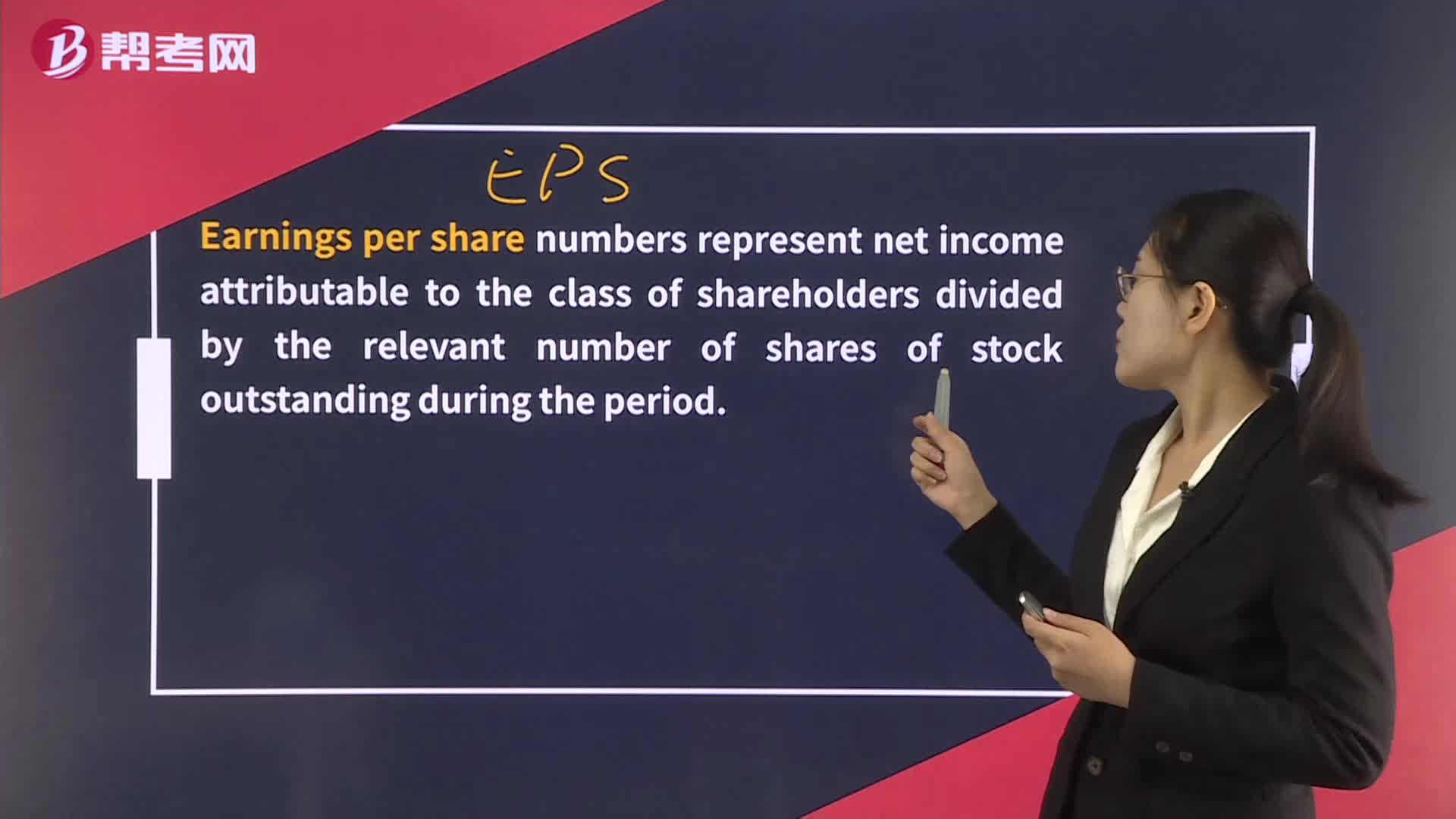

Income Statement– Earnings Per Share

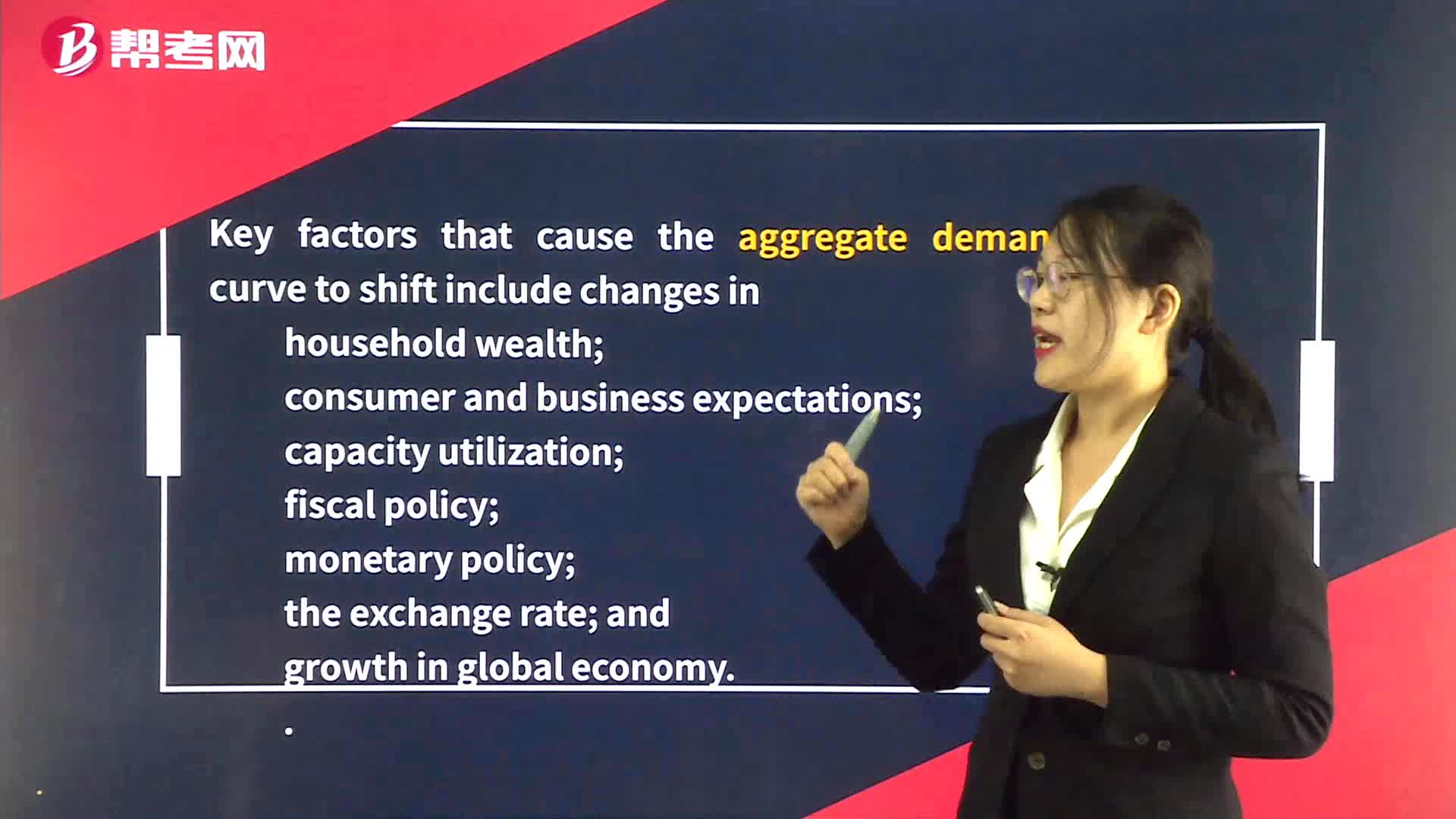

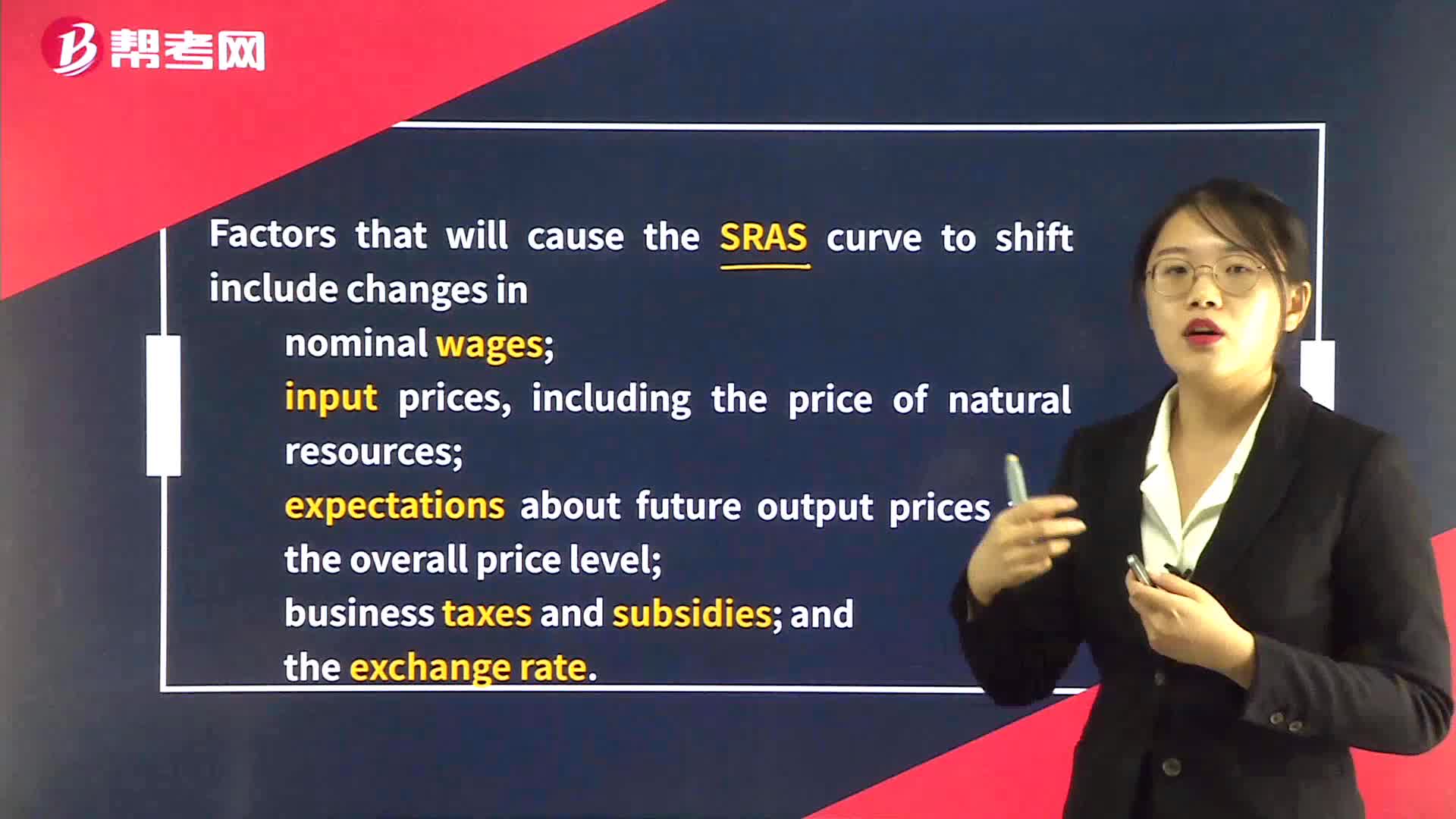

Shifts in Aggregate Supply

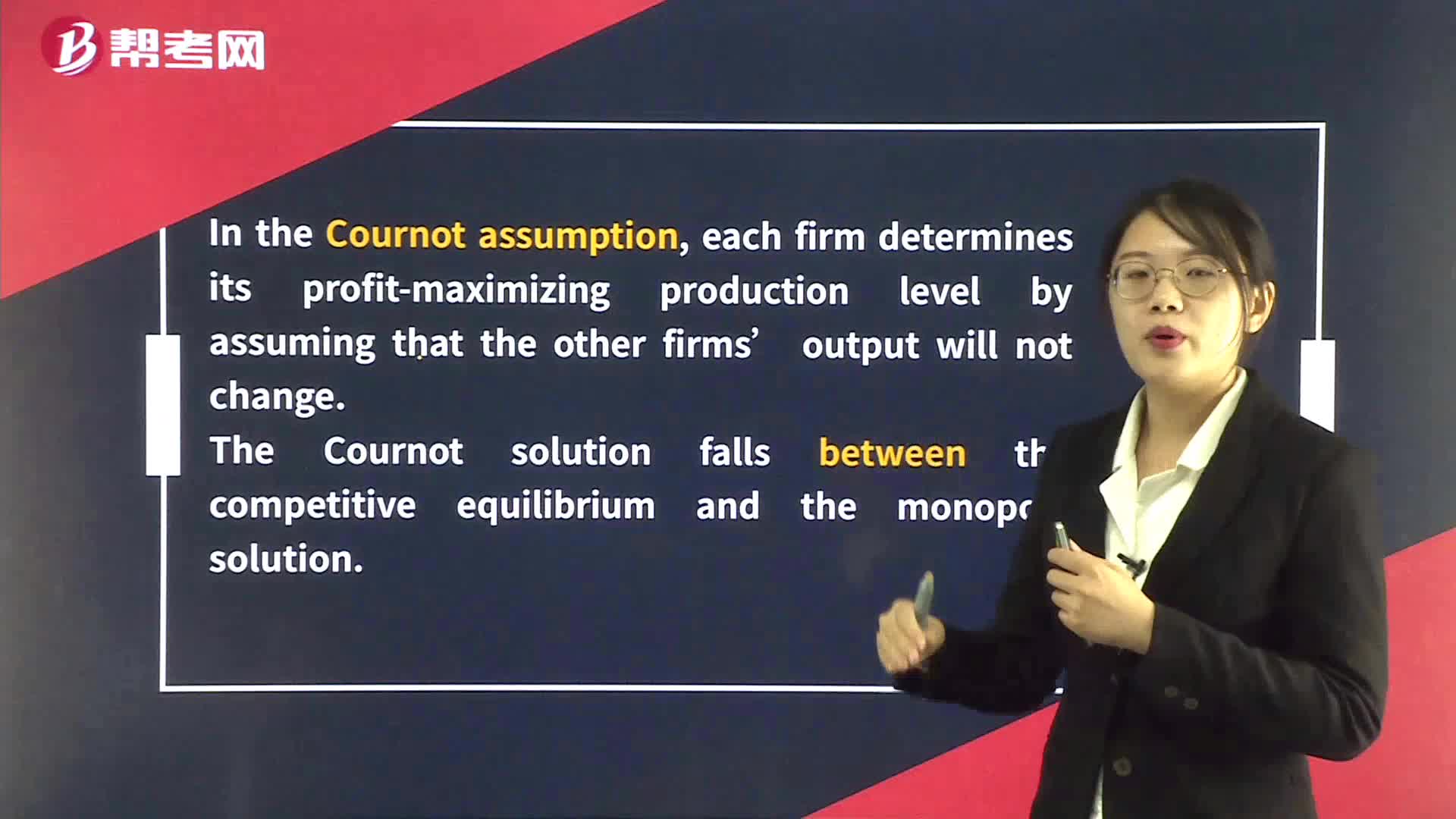

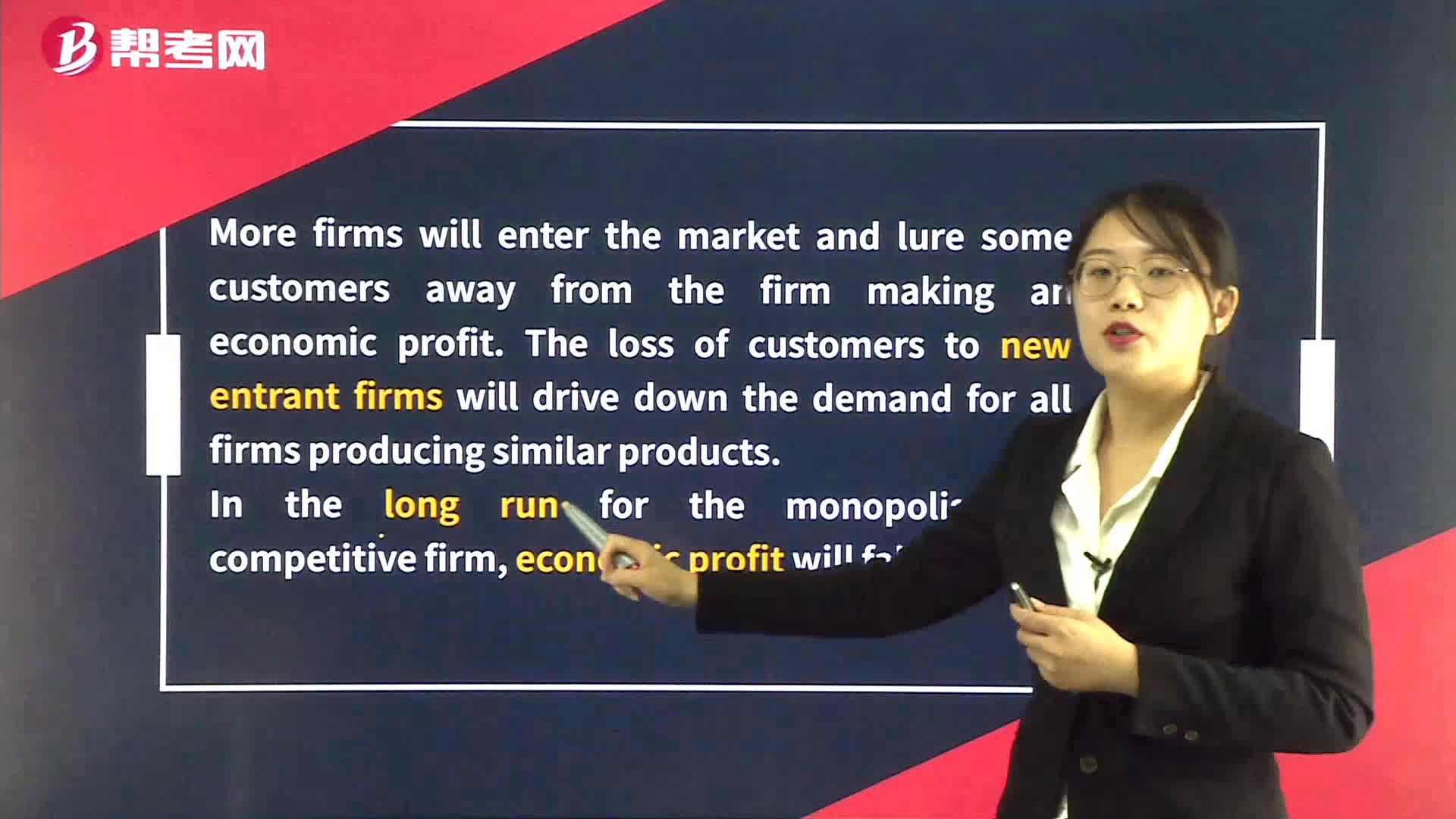

Long-Run Equilibrium in Monopolistic Competition

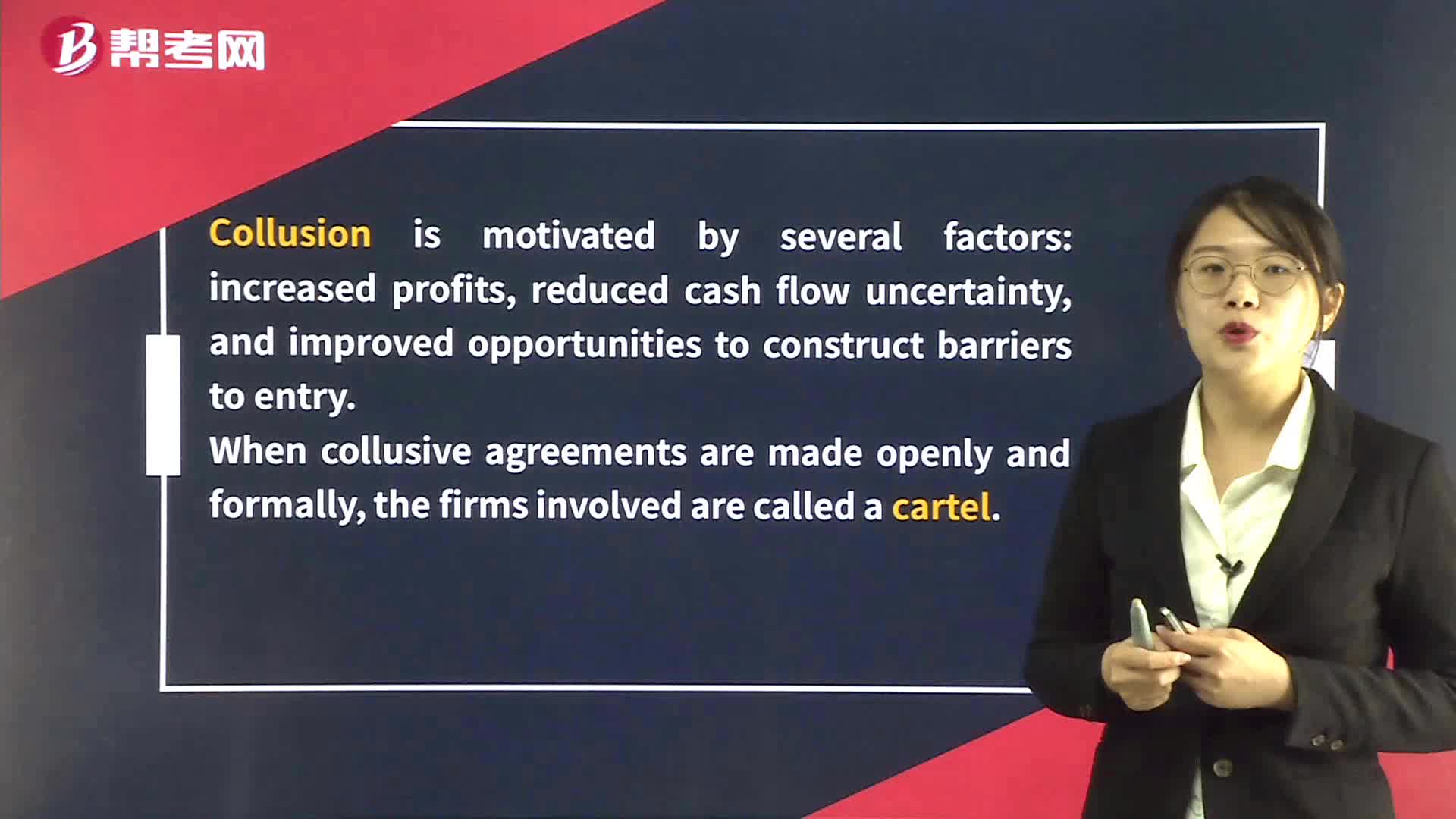

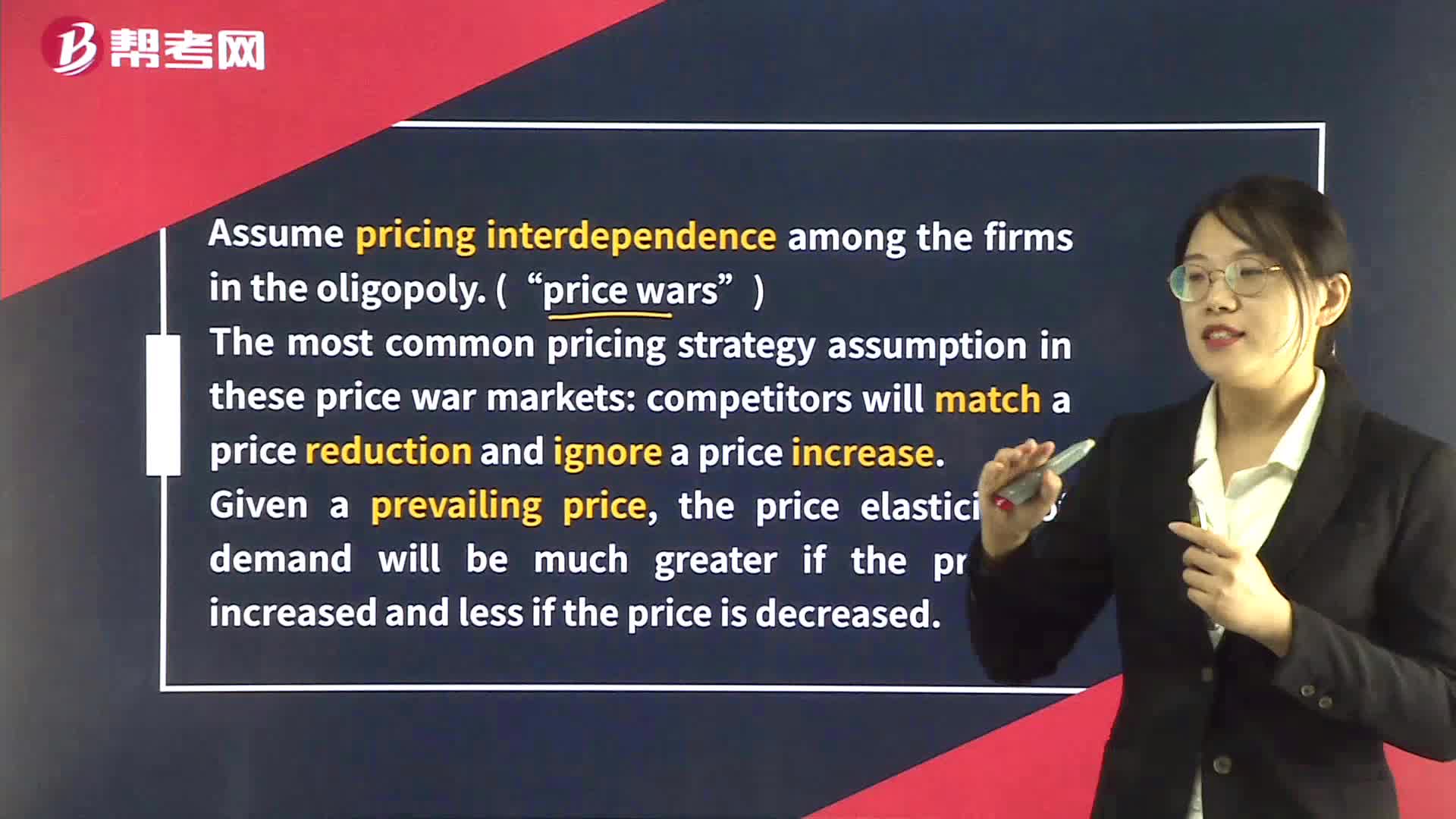

Kinked Demand Curve in Oligopoly Market